Structural Validation Of Synthetic Power Distribution Networks Using The Multiscale Flat Norm

Abstract

We study the problem of comparing a pair of geometric networks that may not be similarly defined, i.e., when they do not have one-to-one correspondences between their nodes and edges. Our motivating application is to compare power distribution networks of a region. Due to the lack of openly available power network datasets, researchers synthesize realistic networks resembling their actual counterparts. But the synthetic digital twins may vary significantly from one another and from actual networks due to varying underlying assumptions and approaches. Hence the user wants to evaluate the quality of networks in terms of their structural similarity to actual power networks. But the lack of correspondence between the networks renders most standard approaches, e.g., subgraph isomorphism and edit distance, unsuitable.

We propose an approach based on the multiscale flat norm, a notion of distance between objects defined in the field of geometric measure theory, to compute the distance between a pair of planar geometric networks. Using a triangulation of the domain containing the input networks, the flat norm distance between two networks at a given scale can be computed by solving a linear program. In addition, this computation automatically identifies the 2D regions (patches) that capture where the two networks are different. We demonstrate through 2D examples that the flat norm distance can capture the variations of inputs more accurately than the commonly used Hausdorff distance. As a notion of stability, we also derive upper bounds on the flat norm distance between a simple 1D curve and its perturbed version as a function of the radius of perturbation for a restricted class of perturbations. We demonstrate our approach on a set of actual power networks from a county in the USA. Our approach can be extended to validate synthetic networks created for multiple infrastructures such as transportation, communication, water, and gas networks.

1 Introduction

The power grid is the most vital infrastructure that provides crucial support for the delivery of basic services to most segments of society. Once considered a passive entity in power grid planning and operation, the power distribution system poses significant challenges in the present day. The increased adoption of rooftop solar photovoltaics (PVs) and electric vehicles (EVs) augmented with residential charging units has altered the energy consumption profile of an average consumer. Access to extensive datasets pertaining to power distribution networks and residential consumer demand is vital for public policy researchers and power system engineers alike. However, the proprietary nature of power distribution system data hinders their public availability. This has led researchers to develop frameworks that synthesize realistic datasets pertaining to the power distribution system [4, 13, 16, 17, 28, 29]. These frameworks create digital replicates similar to the actual power distribution networks in terms of their structure and function. Hence the created networks can be used as digital duplicates in simulation studies of policies and methods before implementation in real systems.

The algorithms associated with these frameworks vary widely—ranging from first principles based approaches [17, 28] to learning statistical distributions of network attributes [29] to using deep learning models such as generative adversarial neural networks [14]. Validating the synthetic power distribution networks with respect to their physical counterpart is vital for assessing the suitability of their use as effective digital duplicates. Since the underlying assumptions and algorithms of each framework are distinct from each other, some of them may excel compared to others in reproducing digital replicates with better precision for selective regions. To this end, we require well-defined metrics to rank the frameworks and judge their strengths and weaknesses in generating digital duplicates of power distribution networks for a particular geographic region.

The literature pertaining to frameworks for synthetic distribution network creation include certain validation results that compare the generated networks to the actual counterpart [4, 12, 29]. But the validation results are mostly limited to comparing the statistical network attributes such as degree and hop distributions and power engineering operational attributes such as node voltages and edge power flows. Since power distribution networks represent real physical systems, the created digital replicates have associated geographic embedding. Therefore, a structural comparison of synthetic network graphs to their actual counterpart becomes pertinent for power distribution networks with geographic embedding. Consider an example where a digital twin is used to analyze impact of a weather event [27]. Severe weather events such as hurricanes, earthquakes and wild fires occur in specific geographic trajectories, affecting only portions of societal infrastructures. In order to correctly identify them during simulations, the digital twin should structurally resemble the actual infrastructure.

Problem Statement: In recent years, the problem of evaluating the quality of reconstructed networks has been studied for street maps. Certain metrics were defined to compare outputs of frameworks that use GPS trajectory data to reconstruct street map graphs [1, 2]. The abstract problem can be stated as follows: compute the similarity between a given pair of embedded planar graphs. This is similar to the well known subgraph isomorphism problem [7] wherein we look for isomorphic subgraphs in a pair of given graphs. A major precursor to this problem is that we require a one-to-one mapping between nodes and edges of the two graphs. While such mappings are well-defined for street networks, the same cannot be inferred for power distribution networks. Since power network datasets are proprietary, the node and edge labels are redacted from the network before it is shared. The actual network is obtained as a set of “drawings” with associated geographic embeddings. Each drawing can be considered as a collection of line segments termed a geometry. Hence the problem of comparing a set of power distribution networks with geographic embedding can be stated as the following: compute the similarity between a given pair of geometries lying on a geographic plane.

Our Contributions: We propose a new distance measure to compare a pair of geometries using the flat norm, a notion of distance between generalized objects studied in geometric measure theory [9, 21]. This distance combines the difference in length of the geometries with the area of the patches contained between them. The area of patches in between the pair of geometries accounts for the lateral displacement between them. We employ a multiscale version of the flat norm [22] that uses a scale parameter to combine the length and area components (for the sake of brevity, we refer to the multiscale flat norm simply as the flat norm). Intuitively, a smaller value of captures larger patches of area between the geometries while a large value of captures more of the (differences in) lengths of the geometries. Computing the flat norm over a range of values of allows us to compare the geometries at multiple scales. For computation, we use a discretized version of the flat norm defined on simplicial complexes [10], which are triangulations in our case. It may not be possible to derive standard stability results for this distance measure that imply only small changes in the flat norm metric when the inputs change by a small amount—there is no alternative metric to measure the small change in the input. We demonstrate through 2D examples (in Fig. 8), for instance, that the commonly used Hausdorff metric cannot be used for this purpose. Instead, we have derived upper bounds on the flat norm distance between a piecewise linear 1-current and its perturbed version as a function of the radius of perturbation under certain assumptions provided the perturbations are performed carefully (see Section 4.3).

A lack of one-to-one correspondence between edges and nodes in the pair of networks prevents us from performing one-to-one comparison of edges. Instead we can sample random regions in the area of interest and compare the pair of geometries within each region. For performing such local comparisons, we define a normalized flat norm where we normalize the flat norm distance between the parts of the two geometries by the sum of the lengths of the two parts in the region. Such comparison enables us to characterize the quality of the digital duplicate for the sampled region. Further, such comparisons over a sequence of sampled regions allows us to characterize the suitability of using the entire synthetic network as a duplicate of the actual network.

Our main contributions are the following: (i) we propose a distance measure for comparing a pair of geometries embedded in the same plane using the flat norm that accounts for deviation in length and lateral displacement between the geometries; and (ii) we perform a region-based characterization of synthetic networks by sampling random regions and comparing the pair of geometries contained within the sampled region. The proposed distance allows us to perform global as well as local comparisons between a pair of network geometries.

1.1 Related Work

Several well defined graph structure comparison metrics such as subgraph isomorphism and edit distance have been proposed in the literature along with algorithms to compute them efficiently. Tantardini et al. [31] compare graph network structures for the entire graph (global comparison) as well as for small portions of the graph known as motifs (local comparison). Other researchers have proposed methodologies to identify structural similarities in embedded graphs [3, 23]. However, all these methods depend on one-to-one correspondence of graph nodes and edges rather than considering the node and edge geometries of the graphs. The edit distance, i.e., the minimum number of edit operations to transform one network to the other, has been widely used to compare networks having structural properties [25, 26, 32]. Riba et al. [26] used the Hausdorff distance between nodes in the network to compare network geometries. Majhi et al. [15] modified the traditional definition of graph edit distance to be applicable in the context of “geometric graphs” embedded in a Euclidean space. Along with the usual insertion and deletion operations, the authors have proposed a cost for translation in computing the geometric edit distance between the graphs. However, the authors also show that the problem of computing this metric is NP-hard.

Meyur et al. [18] compared network geometries using the Hausdorff distance after partitioning the geographic region into small rectangular grids and comparing the geometries for each grid. However, the Hausdorff metric is sensitive to outliers as it focuses only on the maximum possible distance between the pair of geometries. When the geometries coincide almost entirely except in a few small portions, the Hausdorff metric still records the discrepancy in those small portions without accounting for the similarity over the majority of portions. The similar approach used by Brovelli et al. [5] to compare a pair of road networks in a geographic region suffers from the same drawback. This necessitates a well-defined distance metric between networks with geographic embedding [2].

Several comparison methods have been proposed in the context of planar graphs embedded in a Euclidean space [6, 19]. They include local and global metrics to compare road networks. The local metrics characterize the networks based on cliques and motifs, while the global metrics involve computing the efficiency of constructing the infrastructure network. The most efficient network is assumed to be the one with only straight line geometries connecting node pairs. Albeit useful to characterize network structures, these methods are not suitable for a numeric comparison of network geometries.

2 Preliminaries

Definition 2.1 (Geometric graph).

A graph with node set and edge set is said to be a geometric graph of if the set of nodes and the edges are Euclidean straight line segments which intersect (possibly) at their endpoints.

Definition 2.2 (Structurally similar geometric graphs).

Two geometric graphs and are said to be structurally similar at the level of , termed -similar, if for the distance function between the two graphs.

We could consider a given network as a set of edge geometries. Hence we could consider the problem of comparing geometric graphs and as that of comparing the set of edge geometries and . In this paper, we propose a suitable distance that allows us to compare between a pair of geometric graphs or a pair of geometries. We use the multiscale flat norm, which has been well explored in the field of geometric measure theory, to define such a distance between the geometries.

2.1 Multiscale Flat Norm

We use the multiscale simplicial flat norm proposed by Ibrahim et al. [10] to compute the distance between two networks. We now introduce some background for this computation. A -dimensional current (referred to as a -current) is a generalized -dimensional geometric object with orientations (or direction) and multiplicities (or magnitude). An example of a -current is a surface with finite area (multiplicity) and a specific orientation (clockwise or counterclockwise). We use to denote the set of all -currents, and to denote the set of -currents embedded in p. or denotes the -dimensional volume of , e.g., length in 1D or area in 2D. The boundary of , denoted by , is a -current. The multiscale flat norm of a -current , at scale is defined as

| (1) |

where the minimum is taken over all -currents .Computing the flat norm of a 1-current (curve) identifies the optimal 2-current (area patches) that minimizes the sum of the length of current and the area of patch(es) . Fig. 1 shows the flat norm computation for a generic 1D current (blue). The 2D area patches (magenta) are computed such that the expression in Eq. (1) is minimized for the chosen value of that ends up using most of the patch under the sharper spike on the left but only a small portion of the patch under the wider bump to the right.

The scale parameter can be intuitively understood as follows. Rolling a ball of radius on the -current traces the output current and the untraced regions constitute the patches . Hence we observe that for a large , the radius of the ball is very small and hence it traces major features while smoothing out (i.e., missing) only minor features (wiggles) of the input current. But for a small , the ball with a large radius smoothes out larger scale features (bumps) in the current. Note that for smaller , the cost of area patches is smaller in the minimization function and hence more patches are used for computing the flat norm. We can use the flat norm to define a natural distance between a pair of 1-currents and as follows [10].

| (2) |

We compute the flat norm distance between a pair of input geometries (synthetic and actual) as the flat norm of the current where and are the currents corresponding to individual geometries. Let denote the set of all line segments in the input current . We perform a constrained triangulation of to obtain a -dimensional finite oriented simplicial complex . A constrained triangulation ensures that each line segment is an edge in , and that is an oriented -dimensional subcomplex of .

Let and denote the numbers of edges and triangles in . We can denote the input current as a -chain where denotes an edge in and is the corresponding multiplicity. Note that indicates that orientation of and are opposite, denotes that is not contained in , and implies that is oriented the same way as . Similarly, we define the set to be the -chain of and denote it by where denotes a -simplex in and is the corresponding multiplicity.

The boundary matrix captures the intersection of the and -simplices of . The entries of the boundary matrix . If edge is a face of triangle , then is nonzero and it is zero otherwise. The entry is if the orientations of and are opposite and it is if the orientations agree.

We can respectively stack the ’s and ’s in and -length vectors and . The -chain representing is denoted by and is given as . The multiscale flat norm defined in Eq. (1) can be computed by solving the following optimization problem:

| (3) | ||||

| s.t. |

where in Eq. (1) denotes the volume of the -dimensional simplex . We denote volume of the edge as and set it to be the Euclidean length, and volume of a triangle as and set it to be the area of the triangle.

In this work, we consider geometric graphs embedded on the geographic plane and are associated with longitude and latitude coordinates. We compute the Euclidean length of edge as where is the Euclidean normed distance between the geographic coordinates of the terminals of and is the radius of the earth. Similarly, the area of triangle is computed as where is the solid angle subtended by the geographic coordinates of the vertices of .

Using the fact that the objective function is piecewise linear in and , the minimization problem can be reformulated as an integer linear program (ILP) as follows:

| (4a) | ||||

| s.t. | (4b) | |||

| (4c) | ||||

| (4d) | ||||

The linear programming relaxation of the ILP in Eq. (4) is obtained by ignoring the integer constraints Eq. (4d). We refer to this relaxed linear program (LP) as the flat norm LP. Ibrahim et al. [10] showed that the boundary matrix is totally unimodular for our application setting. Hence the flat norm LP will solve the ILP, and hence the flat norm can be computed in polynomial time.

Algorithm 1 describes how we compute the distance between a pair of geometries with the associated embedding on a metric space . We assume that the geometries (networks) and with respective node sets and edge sets have no one-to-one correspondence between the ’s or ’s. Note that each vertex is a point and each edge is a straight line segment in . We consider the collection of edges as input to our algorithm. First, we orient the edge geometries in a particular direction (left to right in our case) to define the currents and , which have both magnitude and direction. Next, we consider the bounding rectangle for the edge geometries and define the set to be triangulated as the set of all edges in either geometry and the bounding rectangle. We perform a constrained Delaunay triangulation [30] on the set to construct the -dimensional simplicial complex . The constrained triangulation ensures that the set of edges in is included in the simplicial complex . Then we define the currents and corresponding to the respective edge geometries and as -chains in . Finally, the flat norm LP is solved to compute the simplicial flat norm.

2.2 Normalized Flat Norm

Recall that in our context of synthetic power distribution networks, the primary goal of comparing a synthetic network to its actual counterpart is to infer the quality of the replica or the digital duplicate synthesized by the framework. The proposed approach using the flat norm for structural comparison of a pair of geometries provides us a method to perform global as well as local comparison. While we can produce a global comparison by computing the flat norm distance between the two networks, it may not provide us with complete information on the quality of the synthetic replicate. On the other hand, a local comparison can provide us details about the framework generating the synthetic networks. For example, a synthetic network generation framework might produce higher quality digital replicates of actual power distribution networks for urban regions as compared to rural areas. A local comparison highlights this attribute and identifies potential use case scenarios of a given synthetic network generation framework.

Furthermore, availability of actual power distribution network data is sparse due to its proprietary nature. We may not be able to produce a global comparison between two networks due to unavailability of network data from one of the sources. Hence, we want to restrict our comparison to only the portions in the region where data from either network is available, which also necessitates a local comparison between the networks.

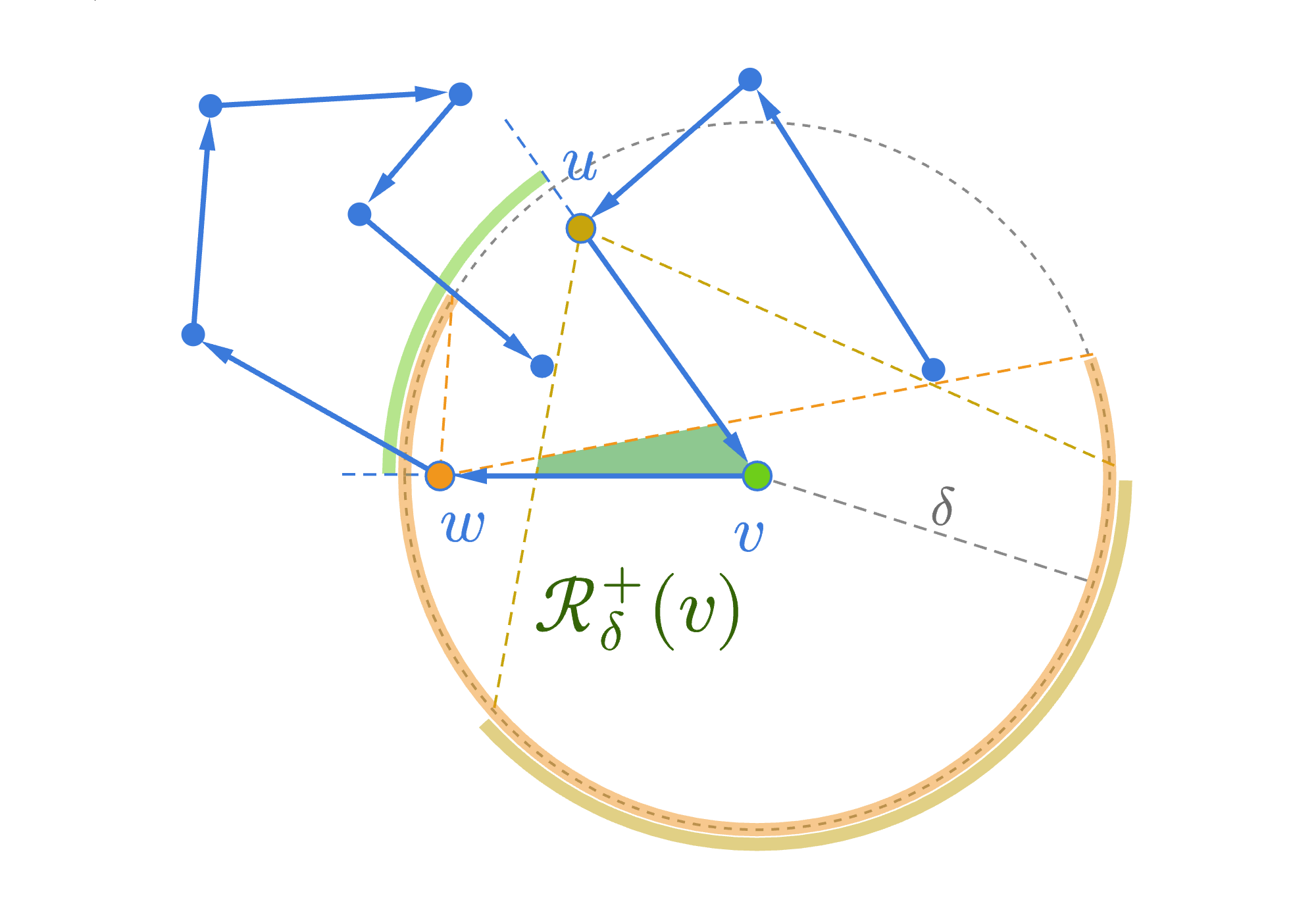

For a local comparison, we consider uniform sized regions and compute the flat norm distance between the pair of geometries within the region. However, the computed flat norm is dependent on the length of edges present within the region from either network. Hence we define the normalized multiscale flat norm, denoted by , for a given region as

| (5) |

For a given parameter , a local region is defined as a square of size steradians. Let and denote the currents representing the input geometries inside the local region characterized by . Note that the “amount” or the total length of network geometries within a square region varies depending on the location of the local region. In this case, the lengths of the network geometries are respectively and . Therefore, we use the ratio of the total length of network geometries inside a square region to the parameter to characterize this “amount” and denote it by where

| (6) |

Note that while performing a comparison between a pair of network geometries in a local region using the multiscale flat norm, we need to ensure that comparison is performed for similar length of the networks inside similar regions. Therefore, the ratio , which indicates the length of networks inside a region scaled to the size of the region, becomes an important aspect of characterization while performing the flat norm based comparison.

3 Implementation of flat norm.

3.1 Geometry comparison using flat norm.

We show a simple example depicting the use of flat norm to compute the distance between a pair of geometries that are two line segments of equal length meeting at their midpoints in Fig. 2. As the angle between the two line segments decreases from to degrees, the computed flat norm also decreases.

3.2 Flat norm computation for a pair of geometries.

We demonstrate the steps involved in computing the flat norm for a pair of input geometries in Fig. 3. The input geometries are a collection of line segments shown in blue and red (top left). We construct the set by combining all the edges of either geometry along with the bounding rectangle (top right). Thereafter, we perform a constrained triangulation to construct the -dimensional simplicial complex (bottom left). Finally, we compute the multiscale simplicial flat norm with (bottom right). Note that this computation captures the length deviation (shown by green edges) and the lateral displacement (shown by the magenta patches).

3.3 Flat norm computation for a pair of networks.

The steps involved in computing the multiscale flat norm distance between a pair of geometries are shown in Fig. 4. They include the actual power distribution network (red) for a region in a county from USA and the synthetic network (blue) constructed for the same region [17]. First, we orient each edge in either network from left to right. Thereafter, we find the enclosing rectangular boundary around the pair of networks. We perform a constrained Delaunay triangulation which ensures that the edges in the geometries and the convex boundary are selected as edges of the triangles. Finally the flat norm LP (relaxation of the ILP in Eq. (4)) is solved to compute the flat norm distance between the networks.

The multiscale flat norm produces different distance values for different values of the scale parameter . Fig. 5 shows the flat norm distance between the actual and synthetic power network for the same region for multiple values of the scale parameter . We observe that as becomes larger, the 2D patches used in computing the flat norm become smaller as it becomes more expensive to use the area term in the flat norm LP minimization problem.

The variation of the computed flat norm for different values of the scale parameter is summarized in Fig. 6. As the scale parameter is increased, fewer area patches are considered in the simplicial flat norm computation. This is captured by the blue decreasing curve in the plot. The computed flat norm increases for larger values of the scale parameter as more and more individual currents contribute their unscaled length toward the flat norm value instead of becoming a boundary of some area component, which, if there are any, now also contribute more because of the increased scale . We show the plot with two different vertical scales: the left scale indicates the deviation in length (measured in km) and the right scale shows the deviation expressed through the area patches (measured in sq.km).

3.4 Comparing Network Geometries

The primary goal of computing the flat norm is to compare the pair of input geometries. As mentioned earlier, the flat norm provides an accurate measure of difference between the geometries by considering both the length deviation and area patches in between the geometries. Further, we normalize the computed flat norm to the total length of the geometries. In this section, we show examples where we computed the normalized flat norm for the pair of network geometries (actual and synthetic) for a few regions.

The top two plots in Fig. 7 show two regions characterized by and almost similar ratios. This indicates that the length of network scaled to the region size is almost equal for the two regions. From a mere visual perspective, we can conclude that the first pair of network geometries resemble each other where as the second pair are fairly different. This is further validated from the results of the flat norm distance between the network geometries computed with the scale , since the first case produces a smaller flat norm distance compared to the latter. The bottom two plots show another example of two regions with almost similar ratios and enable us to infer similar conclusions. The results strengthens our case of using flat norm as an appropriate measure to perform a local comparison of network geometries. We can choose a suitable which differentiates between these example cases and use the proposed flat norm distance metric to identify structurally similar network geometries. However, the choice of has to be made empirically. This necessitates a statistical study of randomly chosen local regions in different sections of the networks, which is performed in the Section 5.

4 Notion of stability for the flat norm distance

We now investigate two approaches to define a notion of stability for the flat norm distance. For any measure of discrepancy between objects, the notion of stability is not only desirable from a theoretical standpoint but is also necessary for practical applications. The comparison metric is said to be stable if small changes in the input geometries lead to only small changes in the measured discrepancy. But such a formulation introduces a “chicken and an egg” problem—in order to evaluate the stability of a proposed metric we need an alternative baseline metric to measure the small change in the input. Of course, the baseline metric should be stable as well. This constitutes the first approach. The alternative approach is to derive directly an upper bound on the proposed metric under well-defined controlled perturbations of input geometries.

The Hausdorff distance metric , which has been extensively used in the literature for comparing geometrically embedded networks, is stable in this sense, and is hence a natural choice for use as the baseline metric. At the same time, the Hausdorff distance is not sensitive enough to adequately measure small changes in the input geometries. Let us consider a -ball around each node in the network for a chosen perturbation radius . We then uniformly sample a point in each circular region and use them as the perturbed embeddings of the nodes. The Hausdorff distance will change if the perturbation is either significantly large to overshadow the current value by moving some node far enough, or it is very specific and affects the maximizer nodes of . As will be shown in the next subsection (Sec. 4.1) on a few simple counter-examples and the real-world networks introduced in the previous section (Sec. 3.3), knowing the value of the Hausdorff distance or how it changed is not enough to infer any useful information about the flat norm distance, and vice versa. Even though our examples are 1-dimensional, the behavior can be observed in any dimension.

In the subsequent subsection (Sec. 4.3), under some mild assumptions about the scale and the radius of perturbation, we derive an upper bound on the flat norm distance for the case of simple piecewise linear curves in 2. We formalize these curves as a special class of integral 1-currents, namely the piecewise linear currents, and study a class of (positive) -perturbations of their nodes. It allows us to track the change of the components of the flat norm distance while perturbing each node one by one, which in turn allows us to construct a non-trivial upper bound on between the original 1-current and its final perturbed version.

4.1 Comparing the Hausdorff and the flat norm distance

We refer the reader to standard textbooks on geometric measure theory [9, 21] for the formal definition of integral currents and other related concepts. For our purposes, it is sufficient to consider an integral current as a collection of oriented manifolds with or without boundary, and with integer multiplicities as well as orientations for each submanifold. Recall from Sec. 2.1 that denotes the set of all oriented -dimensional integral currents (-current) embedded in d+1, and is the -dimensional support for . Let with -boundary , then the set of all -currents embedded in d+1 spanned by the boundary of is denoted as , or simply if the embedding space is clear from the context.

Let be two integral -currents in d+1, and be the Euclidean distance between . The Hausdorff distance between currents and is given by

where is the distance from a point to a current given as

Let be the -component of the flat norm decomposition in Eq. (1). Note that , i.e., , and it can be rendered to zero only if . Hence, the volume of the minimal -current spanned by provides a lower bound on . On the other hand the Hausdorff distance between boundaries doesn’t provide any meaningful insights about the actual value of . This prompts us to suspect that the Hausdorff distance between two -currents does not have any meaningful relations with the value of the flat norm distance. In fact, we expect to be more sensitive to perturbations of input geometries. Moreover, as can be seen from the examples below and the discussion in the following Section 4.3, given that the scale is small enough, when is perturbed within a -tube the range of incurred changes of the flat norm distance depends, mainly, on the size of perturbation and the input volume , and not on . Although the examples in this Section are given for 1-currents in 2 for illustrative purposes, this conclusion holds in the general case of -currents as well.

Example 4.1 (Fixing ).

Let and be two 1-currents in 2 with common boundaries, , and let be the Hausdorff distance between them. For some small , consider —a perturbation of within an -tube—such that the boundaries and the Hausdorff distance do not change:

Note that . See Fig. 8 for examples of perturbations .

We could have cases where lies mostly at the upper envelope of this -tube, causing the flat norm distance to increase by (highlighted in green), or mostly at the lower envelope causing a decrease in the flat norm distance, respectively (highlighted in pink). In both cases, one would expect the ideal measure of discrepancy between and to change significantly as well (compared to the one between and ). The flat norm distance accurately captures all such changes (to keep the example simple, we consider the default flat norm distance and not the normalized version). At the same time, both such variations could have the same Hausdorff distance from as , which completely misses all the changes applied to in either case.

Example 4.2 (Fixing ).

A modification of this example can illustrate the other extreme case—when Hausdorff distance changes by a lot but the flat norm distance does not change much at all, see bottom row in Fig. 8. Consider moving only the highest point on further away from so that Hausdorff distance becomes , as shown on the bottom left figure of Fig. 8. We keep a connected curve, thus creating a sharp spike in it. While the Hausdorff distance between the curves has increased dramatically, the flat norm distance sees only a minute increase as measured by the area under the spike. Moreover, the increment can be decreased to almost zero by narrowing the spike. Once again, the flat norm distance accurately captures the intuition that the curves have not changed much when just a single point moves away while the rest of the curve stays the same. Hence the flat norm provides a more robust metric that better captures significant changes while maintaining stability to small perturbations (also see Section 4.3 for theoretical bounds).

4.2 Empirical study

We observe similar behavior to those illustrated by the theoretical example (Fig. 8) in our computational experiments. Fig. 9 shows scatter plots denoting empirical distribution of percentage deviation of the two metrics from the original values for a local region. The perturbations are considered for three different radii shown in separate plots. We note that the percentage deviations in the two metrics are comparable in most cases. In other words, neither metric behaves abnormally for a small perturbation in one of the networks.

Next, we compare the sensitivity of the two metrics to outliers. Here, we consider a single random node in one of the networks and perturb it. Fig. 10 shows the sensitivity of the metrics to these outliers. The original normalized flat norm and Hausdorff distance metrics are shown by the horizontal and vertical dashed lines respectively. The points along the horizontal dashed line denote the cases where the Hausdorff distance metric is more sensitive to the outliers, while the normalized flat norm metric remains the same. These cases occur when the perturbed random node determines the Hausdorff distance, similar to the second Example where Hausdorff distance increased from to . On the flip side, the points along the vertical dashed line denote the Hausdorff distance remaining unchanged while the normalized flat norm metric shows variation. Just as in the theoretical example (Fig. 8), such variation in the normalized flat norm metric implies a variation in the network structure. However, such variation is not captured by the Hausdorff distance metric. Hence, our proposed metric is capable of identifying structural differences due to perturbations while remaining stable when widely separated nodes (which are involved in Hausdorff distance computation) are perturbed. The other points which are neither on the horizontal nor the vertical dashed lines indicate that either metric can identify the structural variation due to the perturbation.

4.3 Stability of the Flat Norm

The results of the previous subsection are applicable in all dimensions, i.e., one cannot expect to bound changes in the flat norm by small functions of the changes in the Hausdorff distance. In this subsection, we adopt a more direct approach to the investigation of the stability of our discrepancy measure between geometric objects. Our goal is to construct an upper bound on from the bottom up based only on the input geometries and an appropriately defined radius of perturbation. To this end, we consider simple piecewise linear (PWL) curves spanned by a pair of points with no self-intersections embedded in 2. Here, simple means that there is no self intersection or branching in the curve that connects two points. Despite its apparent simplicity, this class of curves is of particular interest, since they can potentially approximate any continuous non-intersecting curve in 2. More directly, power grid networks that form the main motivated for our work can be seen as collections of such simple curves. Although, the results of this subsection are proven only for a pair of simple PWL currents, the empirical findings on the real-world networks, presented in the next section (Sec. 5) comply surprisingly well with the upper bounds established for simple curves (see Fig. 17).

We conceptualize a simple piecewise linear curve between points and as the 1-current embedded in 2 that is equipped with an edge set given by the linear segments of , and a node set , where and , and for . Such currents are defined as a formal sum of their edges , and can be thought of as discretized linear approximations of simple continuous curves in 2. We refer to this type of currents as PWL currents, and denote the set of all PWL currents with edges spanned by and (i.e., starting at and ending and ) as or . A subcurrent of spanned by nodes and , where , is denoted , and , which implies . The length of is given by .

We start with a PWL current in 2 and its copy . Next, we consider a sequence of perturbations of ’s nodes within some -neighborhood to obtain , while tracking the components of the flat norm distance between the original and the perturbed copy. Recall that the components of the flat norm distance between generic inputs and are the perimeter of the unfilled void and the area of a 2-current given as , see Fig. 1. We refer to them as the length (or perimeter) and the area components of flat norm distance, respectively:

| (7) |

Since and are identical to start with, the flat norm distance between them is zero (for ). Now let us take a look at the components of the flat norm distance between the original current and the perturbed copy . Let be the 2-dimensional void with the boundary given by , and be a 2-current that fills in, possibly partially, the void . The area component in the optimal decomposition of is bounded by the area of , , and is maximized when the void is fully filled, i.e., . On the other hand, the length component can be, potentially, arbitrarily large due to the complexity of :

| (8) |

Here we make an important assumption about the values of parameters and , formalized below, that allows us to circumvent the potential unboundedness of the perimeter component. We mention that the problem of identifying the ranges of values of parameters that fit the assumption is out of the scope of this paper, and will be the focus of future research.

Assumption 4.3 (Filled voids).

For any original current embedded in 2, the scale parameter is small enough such that for any size of the perturbation taken within some range , the optimal decomposition of the flat norm distance between and its consecutive perturbations always fills in all the voids that appear as a result of the perturbations.

We note that this assumption does not introduce any additional challenges in implementing the flat norm distance, since we always can find a small enough by scaling it by one-half until all gaps between the input geometries are filled.

Given parameters and under Assumption 4.3, the minimization objective of in Eq. (7) is achieved by a 2-current , where is a 2D-void in between and . Hence, , i.e., . This implies that the length component in Eq. (8) renders to 0—its minimum value. Conversely, if we would leave the void unfilled, i.e., , then the area component as well as its boundary become zero, and , while the length component is equal to the void’s perimeter: . Hence, under Assumption 4.3, the optimization objective of reduces to the scaled area of for :

| (9) |

This collapsed minimization objective implies that for the scale and the perturbation radius given by our assumption, the void produced by perturbing the copy of is filled in by a 2-current spanned by , such that the scaled area of is upper bounded by its (non-scaled) perimeter:

| (10) |

4.3.1 -perturbations of PWL currents

We consider a PWL current spanned by , called the original current, and its copy , e.g., see Fig. 11. Obviously, at any scale .

Let be an interior vertex of , . Given a radius of perturbation , consider a mapping such that stays within an open -ball centered at , i.e., . Let and be the adjacent nodes of , and let the corresponding incident edges be and . Then, let and be the edge-like currents connecting the neighbors of to its perturbation , see Fig. 13. We define a -perturbation of as the collection of mappings of along with its two connected edges under the assumption that the new edges and do not cross any of the original edges.

where is the allowed region of -perturbation defined as a subregion of the -ball centered at that is in the direct line of sight of the vertices adjacent to (see Fig. 12):

| (11) |

A -perturbation of a vertex maps into by acting on its node and edge sets as defined below, and defines a -perturbation . We say that the -perturbation of a current is induced by . Note that the non-overlapping conditions in Eq. (11), implies that , which means that is injective (has no self intersections).

The -perturbations of boundaries are given by the following maps:

where and .

4.3.2 Flat Norm of -perturbations

Having specified the necessary definitions and procedures, we are now ready to prove our first result regarding a single -perturbation of an interior node.

Theorem 4.4.

Let for and be its copy. Given a small enough scale and an appropriate radius of perturbation , consider a -perturbation induced by perturbation of an interior node . Then the flat norm distance between and is upper bounded as follows:

where and are vertices of adjacent to .

Proof.

Recall that by the Assumption 4.3, the optimal 2-current is spanned by , and by the construction of the new edges and do not overlap with the original current. Then , which is the boundary of a quadrilateral spanned by the vertices , see Fig. 13. To keep the notation simple, we just write . Consider the diagonal that connects to its perturbation. Its length is bounded by the radius of perturbation and it partitions into a pair of triangles and :

| (12) |

with boundaries given by and . The corresponding areas are and , where is the angle between the diagonal and the original edge in the corresponding triangle, (see Fig. 13). Note that both and , and consequently , attain the largest possible area when the perturbed vertex lands on the boundary of the -ball and is perpendicular to the original edges, i.e., . Let be one of the triangles and or be its original edge, then the following are the upper bounds on the area of and :

| (13) | ||||

| (14) |

Furthermore, observe that by the triangle inequality (see Fig. 13) the length of the perturbed edges in the boundary of is bounded as follows:

| (15) |

which implies that , and thus the following bounds hold:

4.3.3 Sequential -perturbations

We now want to derive results similar to Theorem 4.4 for the case where perturbations are applied to a subcurrent of given by a subset of its adjacent nodes. To this end, we consider a sequence of -perturbations of the copy current induced by sequential perturbations of the interior points , which we denote as .

The procedure of -perturbations described above does not guarantee “out of the box” additivity of the area components of the corresponding flat norm distances . The problem arises when a -perturbation lands within a region produced by for some , where . It means that and . But since and are embedded in 2 the area of a formal sum is not larger than the area of their union: . Therefore, to find an upper bound for we can consider only perturbation sequences that produce non-overlapping regions , and hence, additive area components .

One way to achieve this is to force for any choice of to land on the same “side” of , and hence of , by restricting the -ball to a positive cone given by the edges incident to in . As an example in Fig. 14, the light green circular arc indicates the segment of the -ball that corresponds to . Let be an interior vertex of , i.e., , and and are the incident edges of in . Then we get that

| (16) |

where for and . In the case of boundary vertices or , the positive cone reduces to the half-disk bounded by a line that contains or , respectively. As previously specified in Eq. (11), the allowed region of is specified by the non-overlapping conditions:

| (17) |

We call a perturbation a positive -perturbation of if . We denote it as , and it induces . It easy to see that a sequence of positive -perturbations produces non-overlapping regions .

Proposition 4.5.

Let for .Consider a sequence of perturbations induced by positive -perturbations of adjacent nodes for some . Then the regions produced by the corresponding perturbations in the sequence do not overlap.

Proof.

First, when two adjacent nodes are perturbed, and , the edge is perturbed twice: , where and . Therefore, the boundaries of corresponding regions and are:

| (18) | ||||

| (19) |

It is worth pointing out that when only interior nodes are perturbed, i.e., and , the edges and are perturbed only once. Thus, the edges incident to the boundaries of , namely and , are perturbed to or if and only if the boundary nodes and were perturbed together with all the nodes in between. In this case the corresponding area components and are given by triangles and , respectively.

Second, observe that any point within is in as well, which means that and . This point also belongs to , since is enclosed by .

Given a sequence , let us assume that for some , while for all . If then and do not share any edges, and hence placing inside requires an intersection of edges, which contradicts . If then and , where , which is also a contradiction. Therefore does not overlap with any of the previously produced regions . ∎

Corollary 4.6 (Additivity of ).

Let for , and is its copy. Given a small enough scale and an appropriate radius of perturbation , consider a sequence of perturbations induced by the positive -perturbations of adjacent nodes in for some . Then the flat norm distance between the adjacent perturbations is additive and sums up to :

where we set .

Proof.

Let be the 2-current that combines all the regions produced by . Since for and , the boundary of is given by

We now present in Theorem 4.7 an upper bound on the flat norm distance between the input current and its perturbed version resulting from a sequence of perturbations of its internal nodes, i.e., nodes in . We subsequently extend the result to include perturbations of all nodes including the boundary nodes in Corollary 4.9.

Theorem 4.7.

Let for , and is its copy. Given a small enough scale and an appropriate radius of perturbation , consider a sequence of perturbations induced by the positive -perturbations of adjacent non-boundary nodes in for some . Then the flat norm distance between and is upper bounded as follows:

Proof.

As previously was observed in Eq. (12), can be partitioned by into a pair of triangles and , with the respective boundaries and . The area of these triangles is bounded as in Eq. (13), and the upper bound on the length of the perturbed edges is given by corresponding triangle inequalities in Eq. 15. Hence, we get the following upper bound for :

| (20) |

Note that the upper bound on the flat norm distance for the first perturbation in the sequence is given by Theorem 4.4 instead of Eq. (20), namely . As was shown above in the Corollary 4.6 under the Assumption 4.3, we get additivity of the flat norm distances between consecutive perturbations, and hence the additivity of the upper bounds. Then we get the Theorem’s claim after doing some algebra:

∎

We immediately get the flat norm bounds on the positive -perturbations of all interior nodes, as well as for perturbations of all nodes as corollaries.

Corollary 4.8 (Complete perturbation of interior).

Given the setup of Theorem 4.7, consider a sequence of perturbations induced by the positive -perturbations of all interior nodes . Then an upper bound on is given by

Corollary 4.9 (Complete perturbation of ).

Given the setup of Theorem 4.7 with , consider a sequence of perturbations induced by the positive -perturbations of each node of . Then an upper bound on is given by

| (21) |

Proof.

Due to the additivity of the flat norm distance between adjacent -perturbations, we can perturb the interior nodes first, and the boundary nodes after that, since now all edges will be perturbed twice and the order will not affect the upper bound. The perturbation of the interior nodes induces a sequence from Corollary 4.8, while induces .

The area components produced by and are spanned by the differences of corresponding perturbations are given by triangles and . Their boundaries are:

| and |

where such that , see Fig. 16. Then the upper bound on the flat norm distance becomes

| (22) | ||||

∎

4.3.4 Normalized flat norm of -perturbations

Recall from Section 2.2 (Eq. (5)) that the normalized flat norm distance is given as

Note that the normalized flat norm distance has a natural upper bound given by that may be of interest when measurements of one of the input geometries are not available or are not reliable. The following corollary of Theorem 4.7 follows from Eq. (21) by dividing both sides by .

Corollary 4.10.

Given the setup of Theorem 4.7 for , consider a sequence of perturbations induced by the positive -perturbations of each node of . Then an upper bound on the normalized flat norm distance is given by

where is the average edge length of .

Theorem 4.11.

Let for , and be its copy. Given a small enough scale and an appropriate radius of perturbation , consider a sequence of perturbations induced by the positive -perturbations of each node of . Then an upper bound on the normalized flat norm distance is given by

| (23) |

where is the average length of perturbed edges.

Proof.

To derive an upper bound for the normalized flat norm distance observe that by the triangle inequality in and we get the following bounds:

Let . Note that and . We then continue the derivation from the intermediate result in Eq. (22) obtained during the proof of Corollary 4.9 of Theorem 4.7:

Recall that . Then,

∎

Combining the generic upper bound in Eq. (10) that holds for small enough and an appropriate , we can rewrite Eq. (23) as

| (24) |

Corollary 4.12.

In the case of a non-shrinking perturbation sequence such that , the upper bound on the normalized flat norm distance is given as

5 Statistical analysis of normalized flat norm

We use the proposed multiscale flat norm to compare a pair of network geometries from power distribution networks for a region in a county in USA. The two networks considered are the actual power distribution network for the region and the synthetic network generated using the methodology proposed by Meyur et al. [17]. We provide a brief overview of these networks.

Actual network. The actual power distribution network was obtained from the power company serving the location. Due to its proprietary nature, node and edge labels were redacted from the shared data. Further, the networks were shared as a set of handmade drawings, many of which had not been drawn to a well-defined scale. We digitized the drawings by overlaying them on OpenStreetMaps [24] and georeferencing to particular points of interest [8]. Geometries corresponding to the actual network edges are obtained as shape files.

Synthetic network. The synthetic power distribution network is generated using a framework with the underlying assumption that the network follows the road network infrastructure to a significant extent [17]. To this end, the residences are connected to local pole top transformers located along the road network to construct the low voltage (LV) secondary distribution network. The local transformers are then connected to the power substation following the road network leading to the medium voltage (MV) primary distribution network. That is, the primary network edges are chosen from the underlying road infrastructure network such that the structural and power engineering constraints are satisfied.

In this section we study the empirical distribution of the normalized flat norm for different local regions and argue that it indeed captures the similarity between input geometries. We use Algorithm (2) to sample random square shaped regions of size steradians from a given geographic location.

We perform our empirical studies for two urban locations of a county in USA. These locations have been identified as ‘Location A’ and ‘Location B’ for the remainder of this paper. We consider local regions of sizes characterized by . For each location, we randomly sample local regions for each value of using Algorithm (2) and hence we consider regions. For every sampled region, we use Algorithm (1) to compute the multiscale flat norm between the network geometries contained within the region with scale parameter . Thereafter, we normalize the computed flat norm using Eq. (5). Additionally, we compute the global normalized flat norm for the entire location and indicate it by . The corresponding square box bounding the entire location is characterized by . We also denote the total length of networks in each location scaled by the size of the location by the ratio . The detailed statistical results for the experiments are included in the Appendix.

5.1 Empirical distribution of

First, we show the histogram of normalized flat norms for Location A and Location B with the five different values for the scale parameter , Fig. 17. Each histogram shows the empirical distribution of normalized flat norm values for uniformly sampled local regions ( regions for each ). We also record the global normalized flat norm between the network geometries of the location and denote it by the solid blue line in each histogram. We show the mean normalized flat norm using the solid green line, with dashed green lines indicating the standard deviation of the distribution. As we can see from the above histograms, the distribution is skewed toward the right for high values of the scale parameter . This follows from our previous discussion of the dependence of the flat norm on the scale parameter: for a large , the area patches are weighed higher in the objective function of the flat norm LP (Eq. (4)). Therefore, the contribution of lengths of the input currents and towards the flat norm distance becomes more dominant at the high values of the scale parameter , so that the flat norm is slowly approaching the total network length . Hence, the normalized flat norm is approaching . For the remainder of the paper, we will continue our discussion with scale parameter since the empirical distributions of normalized flat norm corresponding to indicate almost Gaussian distribution.

Next, we consider the empirical distribution of normalized flat norm computed with scale parameter for uniformly sampled local regions in Location A and Location B, Fig. 18. We show separate histograms for four different-sized local regions (different values of ). Note that for small-sized local regions (low ), the distribution is skewed toward the right. This is because when we consider small regions, we often capture very isolated network geometries and the flat norm computation is close to the total network length , which again leads the normalized flat norm to be close to . Such occurrences are avoided in larger local regions, and therefore we do not observe skewed distributions.

5.2 Distribution of across local regions

The scatter plot in the top left of Fig. 19 shows the empirical distribution of values. The scatter plot highlights as a blue star the global value of Location A, which indicates the normalized flat norm computed for the entire location. The global normalized flat norm (with a scale parameter ) for Location A is and the ratio . Further, nine additional points are highlighted in the scatter plot denoting nine local regions within Location A. The solid green line denotes the mean of the normalized flat norm values and the dashed green lines indicate the spread of the values around the mean.

The nine local regions are selected such that three of them have the minimum in the location (highlighted by cyan colored diamonds), three of them have the maximum in the location (highlighted by purple triangles), and the remaining three local regions have the values close to the global value for the location (highlighted by tan plus symbols). The network geometries within each region and the flat norm computation with scale are shown in the bottom plots. The computed flat norm and ratio values are shown above each plot. The local regions are also highlighted (cyan, purple, and tan colored boxes, respectively) in the top right plot where the actual and synthetic network geometries within the entire location are overlaid. Fig. 20 shows similar local regions from Location B.

From a mere visual inspection of both Figs. 19 and 20, we notice that the network geometries in each local region shown in the first row of the bottom plots resemble and almost overlap each other. The computed normalized flat norm values for these local regions agree with this observation. Similarly, the large value of the normalized flat norm justifies the observation that network geometries for local regions depicted in the second row of the bottom plots do not resemble each other. These observations validate our choice of using normalized flat norm as a suitable measure to compare network geometries for local regions.

6 Conclusions

We have proposed a fairly general metric to compare a pair of network geometries embedded on the same plane. Unlike standard approaches that map the geometries to points in a possibly simpler space and then measuring distance between those points [11], or comparing “signatures” for the geometries, our metric works directly in the input space and hence allows us to capture all details in the input. The metric uses the multiscale flat norm from geometric measure theory, and can be used in more general settings as long as we can triangulate the region containing the two geometries. It is impossible to derive standard stability results for this distance measure that imply only small changes in the flat norm metric when the inputs change by a small amount—there is no alternative metric to measure the small change in the input. For instance, our theoretical example (in Fig. 8) shows that the commonly used Hausdorff metric cannot be used for this purpose. Instead, we have derived upper bounds on the flat norm distance between a piecewise linear 1-current and its perturbed version as a function of the radius of perturbation under certain assumptions provided the perturbations are performed carefully (see Section 4.3). On the other hand, we do get natural stability results for our distance following the properties of the flat norm—small changes in the input geometries lead to only small changes in the flat norm distance between them [9, 20].

We use the proposed metric to compare a pair of power distribution networks: (i) actual power distribution networks of two locations in a county of USA obtained from a power company and (ii) synthetically generated digital duplicate of the network created for the same geographic location. The proposed comparison metric is able to perform global as well as local comparison of network geometries for the two locations. We discuss the effect of different parameters used in the metric on the comparison. Further, we validate the suitability of using the flat norm metric for such comparisons using computation as well as theoretical examples.

References

- [1] Mahmuda Ahmed, Brittany Terese Fasy, Kyle S. Hickmann, and Carola Wenk. A path-based distance for street map comparison. ACM Trans. Spatial Algorithms Syst., 1(1), 2015.

- [2] Mahmuda Ahmed, Brittany Terese Fasy, and Carola Wenk. Local persistent homology based distance between maps. In Proceedings of the 22nd ACM SIGSPATIAL International Conference on Advances in Geographic Information Systems, SIGSPATIAL ’14, page 43–52, New York, NY, USA, 2014. Association for Computing Machinery.

- [3] Yunsheng Bai, Hao Ding, Song Bian, Ting Chen, Yizhou Sun, and Wei Wang. SimGNN: A Neural Network Approach to Fast Graph Similarity Computation. In Proceedings of the Twelfth ACM International Conference on Web Search and Data Mining, WSDM ’19, page 384–392, New York, NY, USA, 2019. Association for Computing Machinery.

- [4] Antoine Bidel, Tom Schelo, and Thomas Hamacher. Synthetic distribution grid generation based on high resolution spatial data. In 2021 IEEE International Conference on Environment and Electrical Engineering and 2021 IEEE Industrial and Commercial Power Systems Europe (EEEIC / ICPS Europe), pages 1–6, Bari, Italy, 2021. IEEE.

- [5] Maria Antonia Brovelli, Marco Minghini, Monia Molinari, and Peter Mooney. Towards an automated comparison of openstreetmap with authoritative road datasets. Transactions in GIS, 21(2):191–206, 2017.

- [6] Alessio Cardillo, Salvatore Scellato, Vito Latora, and Sergio Porta. Structural properties of planar graphs of urban street patterns. Phys. Rev. E, 73:066107, 2006.

- [7] David Eppstein. Subgraph isomorphism in planar graphs and related problems. In Proceedings of the Sixth Annual ACM-SIAM Symposium on Discrete Algorithms, SODA ’95, page 632–640, USA, 1995. Society for Industrial and Applied Mathematics.

- [8] ESRI. Georeferencing a raster to a vector, 2022. https://desktop.arcgis.com/en/arcmap/ latest/manage-data/raster-and-images/georeferencing-a-raster-to-a-vector.html; last accessed 26 Sept 2022.

- [9] Herbert Federer. Geometric Measure Theory. Die Grundlehren der mathematischen Wissenschaften, Band 153. Springer-Verlag, New York, 1969.

- [10] Sharif Ibrahim, Bala Krishnamoorthy, and Kevin R. Vixie. Simplicial flat norm with scale. Journal of Computational Geometry, 4(1):133–159, 2013. arXiv:1105.5104.

- [11] David G. Kendall, Dennis M. Barden, T. Keith Carne, and Huiling Le. Shape and Shape Theory. Wiley Series in Probability and Statistics. Wiley, Hoboken, NJ, USA, 2009.

- [12] Venkat Krishnan, Bruce Bugbee, Tarek Elgindy, Carlos Mateo, Pablo Duenas, Fernando Postigo, Jean-Séebastien Lacroix, Tomás Gómez San Roman, and Bryan Palmintier. Validation of synthetic u.s. electric power distribution system data sets. IEEE Transactions on Smart Grid, 11(5):4477–4489, 2020.

- [13] Hanyue Li, Jessica L. Wert, Adam Barlow Birchfield, Thomas J. Overbye, Tomas Gomez San Roman, Carlos Mateo Domingo, Fernando Emilio Postigo Marcos, Pablo Duenas Martinez, Tarek Elgindy, and Bryan Palmintier. Building highly detailed synthetic electric grid data sets for combined transmission and distribution systems. IEEE Open Access Journal of Power and Energy, 7:478–488, 2020.

- [14] Ming Liang, Yao Meng, Jiyu Wang, David L. Lubkeman, and Ning Lu. Feedergan: Synthetic feeder generation via deep graph adversarial nets. IEEE Transactions on Smart Grid, 12(2):1163–1173, 2021.

- [15] Sushovan Majhi and Carola Wenk. Distance measures for geometric graphs. Computational Geometry, 118:102056, 2024.

- [16] Carlos Mateo, Fernando Postigo, Fernando de Cuadra, Tomás Gómez San Roman, Tarek Elgindy, Pablo Dueñas, Bri-Mathias Hodge, Venkat Krishnan, and Bryan Palmintier. Building large-scale u.s. synthetic electric distribution system models. IEEE Transactions on Smart Grid, 11(6):5301–5313, 2020.

- [17] Rounak Meyur, Madhav Marathe, Anil Vullikanti, Henning Mortveit, Samarth Swarup, Virgilio Centeno, and Arun Phadke. Creating realistic power distribution networks using interdependent road infrastructure. In 2020 IEEE International Conference on Big Data (Big Data), pages 1226–1235, Atlanta, GA, USA, 2020. IEEE.

- [18] Rounak Meyur, Anil Vullikanti, Samarth Swarup, Henning Mortveit, Virgilio Centeno, Arun Phadke, Vince Poor, and Madhav Marathe. Ensembles of realistic power distribution networks. Proceedings of the National Academy of Sciences, 119(26):e2123355119, 2022.

- [19] Ignacio Morer, Alessio Cardillo, Albert Díaz-Guilera, Luce Prignano, and Sergi Lozano. Comparing spatial networks: A one-size-fits-all efficiency-driven approach. Phys. Rev. E, 101:042301, 2020.

- [20] Frank Morgan. Geometric Measure Theory: A Beginner’s Guide. Academic Press, Cambridge, MA, USA, fourth edition, 2008.

- [21] Frank Morgan. Geometric Measure Theory: A Beginner’s Guide. Academic Press, Cambridge, MA, USA, 5th edition, 2016.

- [22] Simon P. Morgan and Kevin R. Vixie. TV computes the flat norm for boundaries. Abstract and Applied Analysis, 2007:Article ID 45153,14 pages, 2007. arXiv:0612287.

- [23] Seongmin Ok. A graph similarity for deep learning. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 1–12, Vancouver, BC, Canada, 2020. Curran Associates, Inc.

- [24] Open Street Map Foundation. Open Street Maps, 2022. www.openstreetmap.org; Last accessed 20 Aug 2022.

- [25] Benjamin Paaßen, Claudio Gallicchio, Alessio Micheli, and Barbara Hammer. Tree edit distance learning via adaptive symbol embeddings. In Jennifer Dy and Andreas Krause, editors, Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 3976–3985. PMLR, 10–15 Jul 2018.

- [26] Pau Riba, Andreas Fischer, Josep Lladós, and Alicia Fornés. Learning graph edit distance by graph neural networks. Pattern Recognition, 120:108132, 2021.

- [27] Kamol Chandra Roy, Samiul Hasan, Aron Culotta, and Naveen Eluru. Predicting traffic demand during hurricane evacuation using real-time data from transportation systems and social media. Transportation Research Part C: Emerging Technologies, 131:103339, 2021.

- [28] Shammya Shananda Saha, Eran Schweitzer, Anna Scaglione, and Nathan G. Johnson. A framework for generating synthetic distribution feeders using openstreetmap. In 2019 North American Power Symposium (NAPS), pages 1–6, Wichita, KS, USA, 2019. IEEE.

- [29] Eran Schweitzer, Anna Scaglione, Antonello Monti, and Giuliano Andrea Pagani. Automated generation algorithm for synthetic medium voltage radial distribution systems. IEEE Journal on Emerging and Selected Topics in Circuits and Systems, 7(2):271–284, 2017.

- [30] Hang Si. Constrained Delaunay tetrahedral mesh generation and refinement. Finite Elements in Analysis and Design, 46:33–46, 2010.

- [31] Mattia Tantardini, Francesca Ieva, Lucia Tajoli, and Carlo Piccardi. Comparing methods for comparing networks. Scientific Reports, 9(1):17557, 2019.

- [32] Hangjun Xu. An algorithm for comparing similarity between two trees. https://arxiv.org/abs/1508.03381, 2015. Last accessed 26 Sept 2022.