On the pitchfork bifurcation of the folded node and other unbounded time-reversible connection problems in

Abstract.

In this paper, we revisit the folded node and the bifurcations of secondary canards at resonances . In particular, we prove for the first time that pitchfork bifurcations occur at all even values of . Our approach relies on a time-reversible version of the Melnikov approach in [27], used in [28] to prove the transcritical bifurcations for all odd values of . It is known that the secondary canards produced by the transcritical and the pitchfork bifurcations only reach the Fenichel slow manifolds on one side of each transcritical bifurcation for all . In this paper, we provide a new geometric explanation for this fact, relying on the symmetry of the normal form and a separate blowup of the fold lines. We also show that our approach for evaluating the Melnikov integrals of the folded node – based upon local characterization of the invariant manifolds by higher order variational equations and reducing these to an inhomogeneous Weber equation – applies to general, quadratic, time-reversible, unbounded connection problems in . We conclude the paper by using our approach to present a new proof of the bifurcation of periodic orbits from infinity in the Falkner-Skan equation and the Nosé equations.

| Department of Applied Mathematics and Computer Science, |

| Technical University of Denmark, |

| 2800 Kgs. Lyngby, |

| DK |

1. Introduction

In slow-fast systems with one fast variable and two slow ones, the folded node is a singularity of the slow flow on the fold line of a critical manifold . See an illustration in Fig. 1. Upon desingularization corresponds to a stable node with eigenvalues , and its strong stable manifold , tangent to the eigenvector associated with , produces a funnel region on the critical manifold, where orbits approach the singularity tangent to the weak eigendirection (associated with the eigenvalue ). Due to the contraction within the funnel region, the folded node – upon composition with a global return mapping – provides a mechanism for producing attracting limit cycles , see [2]. In fact, a blowup of the folded node reveals one orbit , along which extended versions and of the attracting and repelling critical manifolds, respectively, twist or rotate; the number of rotations being described by . The twisting is such that these manifolds intersect transversally whenever . As a consequence, for these values of , there exists a ‘weak canard’ connecting extended versions of the Fenichel slow manifolds. This orbit acts, due to the twisting of along , as a ‘center of rotation’ and trajectories on either side will therefore experience small oscillations before they leave a neighborhood of by following its unstable set; in Fig. 1 this unstable set coincides with the positive -axis. Consequently, the limit cycles will be of mixed-mode type where small oscillations are followed by larger ones. Such oscillations appear in many applications, perhaps most notably in chemical reaction dynamics, and the folded node has therefore gained glory as a (relatively) simple mathematical model of this phenomenon, see e.g. the review article [4].

Bifurcations of the weak canard occurs whenever ; in this case, for , the twisting of and is such that these manifolds intersect tangentially along . These bifurcations were described for by the reference [28], working on the ‘normal form’

| (1.1) | ||||

and using the Melnikov approach developed in [27], following [26]. The system (1.1) is related to the blowup of the folded node for . In particular for (1.1), takes the following form

| (1.2) |

For each odd , it was shown that there is a transcritical bifurcation of ‘canards’ connecting and . For all , this bifurcation produces additional transversal intersections of the slow manifold. The resulting new canards – the ‘secondary canards’ – produce bands on the attracting slow manifold where different number of small oscillations occur, see [2, 4, 28]. For any even , it was conjectured that a pitchfork bifurcation occurs. This was supported by numerical computations. Furthermore, in [18, App. A] a way was found to compute a ‘third order’ Melnikov integral using Mathematica for all even and explicit computations demonstrated that the integral was nonzero for even values of up to . Following the work of [28] this also shows that a pitchfork bifurcation occurs, at least for these values.

In this paper, we prove the pitchfork bifurcation for every even by evaluating the third order Melnikov integral analytically. Our approach is based upon a time-reversible version of the Melnikov theory of [27]. However, the most important insight of this paper is to characterize the manifolds and locally by solutions to higher order variational equations; this is in contrast to [28] which uses an integral representation of these manifolds. We show that this approach, relying on reducing these variational equations to an inhomogeneous Weber equation, extends to a very general class of time-reversible, quadratic, unbounded connection problems in . Regardless, for the folded node the ‘time-reversible approach’ also allows us to provide a more detailed blowup picture of the folded node, including a rigorous description of the additional transverse intersections of and that arise due to the pitchfork bifurcation.

The bifurcations of canards for (1.1), is closely related to bifurcations of periodic orbits from heteroclinic cycles at infinity. The Falkner-Skan equation

| (1.3) |

and the Nosé equation:

| (1.4) | ||||

are well-known examples of systems (without equilibria) possessing such bifurcations, see e.g. [23], and [17] for other examples. The Falkner-Skan equation (1.3) initially appeared in the study of boundary layers in fluid dynamics, see [6]. In this context, the physical relevant parameter regime is . However, the equation has subsequently been studied by other authors [22, 21, 23] for all on the basis of the rich dynamics it possesses (including chaotic dynamics and a novel bifurcation of periodic orbits from infinity). On the other hand, the Nosé equations (1.4) model the interaction of a particle with a heat bath [19]. The system also has interesting dynamics without any equilibrium and possesses many similar properties to (1.1) and (1.3). Nevertheless, the description of the bifurcating periodic orbits in both of these systems, is – as noted by [23] – long and cumbersome, and to a large extend, independent of standard methods of dynamical systems theory. Therefore, although the folded node will be our primary focus, a subsequent aim of the paper, is to apply the Melnikov theory, and our classification of and through solutions of an inhomogeneous Weber equation, to these bifurcations and present a simpler description of the emergence of periodic orbits, based on normal form theory and invariant manifolds and therefore more in tune with dynamical systems theory.

1.1. The folded node: Further background

Following [28, Proposition 2.1], any folded node can be brought into the ‘normal form’:

| (1.5) | ||||

by only using scalings, translations and a regular time transformation. Here , and the critical manifold is approximately given by the parabolic cylinder , () being stable and () being unstable. See Fig. 1. Here is in blue, is in red, whereas the degenerate line , being the fold line, is in green. For (1.5), the folded node (pink), on , is at the origin. Furthermore, if we for simplicity ignore the -terms in (1.5), then the reduced problem on is given by

Consider where . Then multiplication of the right hand side by gives the topologically equivalent system

| (1.6) | ||||

on , see [28]. The point is then a stable node of these equations with eigenvalues and and associated eigenvectors:

| (1.7) |

and , respectively. See illustration of the reduced flow in Fig. 2. Notice that the orbits on , where , are also orbits of (1.6), but their directions have to be reversed.

Blowup analysis

Compact submanifolds (with boundaries) and of and , respectively, bounded away from the fold line, perturb by Fenichel’s theory to attracting and repelling slow manifolds and for all , see [7, 8, 9, 12]. We will refer to these manifolds as ‘Fenichel’s (slow) manifolds’. They are nonunique but -close. Extended versions of these invariant manifolds up close to the folded node is obtained in [24] by blowing up the point for . In further details, the authors apply the following blowup transformation , given by

| (1.8) |

to the extended system . For this extended system, is fully nonhyperbolic – its linearization having only zero eigenvalues – but upon blowup (1.8), we gain hyperbolicity of after desingularization through division of the resulting right hand sides by . In particular, setting in (1.8) produces the following local form of (1.8)

| (1.9) |

The local coordinates provide a coordinate chart ‘’, covering where . Here corresponds to . In this chart, one gains hyperbolicity of and for upon division of the right hand side by . By center manifold theory, this then enables an extension of the Fenichel slow manifolds and as the -image of const. sections of three-dimensional invariant manifolds and , respectively, for all . Following [16], we shall abbreviate these extended manifolds in the -space by and , respectively; see [24] for further details.

Remark 1.1.

It is important to highlight that, due to the contraction towards the weak canard, the forward (backward) flow of the Fenichel manifold (, respectively) is only a subset of (). Therefore when we intersect and , extended by the forward and backward flow, it does not follow directly that the Fenichel manifolds and also intersect.

Notice that the blowup approach, following (1.9) and the conservation of , provide control of and up to -close to the folded node , justifying the use of the subscripts. To describe these manifolds beyond this, we have to look at the (scaling) chart obtained by setting . This produces the following local blowup transformation

| (1.10) |

using the chart-specified coordinates . The corresponding coordinate chart ‘’ covers where . By inserting (1.10) into (1.5), dividing the right hand side by and subsequently setting , we obtain (1.1), repeated here for convenience:

| (1.11) | ||||

In (1.11), we have also dropped the subscripts on . Two explicit algebraic solutions are known for this unperturbed system, one:

corresponding to the ‘strong canard’, while in (1.2), repeated here for convenience:

| (1.12) |

corresponds to the ‘weak canard’, which we will focus on in this paper.

Remark 1.2.

Notice that the projection of (1.12) onto the -plane coincides with the span of the weak eigenvector (1.7), explaining the use of ‘weak’ in ‘weak canard’. Also, the orbit (1.12) is unique as an orbit on the blowup sphere with these properties. This is obviously in contrast with reduced flow on where all trajectories within the funnel is assumption to the weak canard.

On a related issue, notice we abuse notation slightly: Most often, will refer to (1.12) as an orbit of (1.11). But by the coordinate chart ‘’, this orbit also becomes a heteroclinic connection on , connecting partially hyperbolic points on the equator for the blowup system. We will use the same symbol for this orbit. At the same time, in Fig. 2 we also use the symbol to highlight the weak eigendirection of the folded node as an attracting node of the desingularized reduced problem on . A similar misuse of notation occurs for .

Restricting the center manifolds and , obtained in the chart , to we obtain, when writing the result in the chart , center-stable and center-unstable manifolds of (1.11) and , respectively, consisting of solutions that grow algebraically as , respectively. Following [24], a simple calculation shows that takes the local form:

| (1.13) |

for all sufficiently large and some smooth for an appropriate interval and sufficiently small. Due to the invariance of and , also satisfies . By using the time-reversible symmetry of (1.11), a simple calculation shows that the manifold takes an identical form, with the expression in (1.13) now valid for all sufficiently negative. We illustrate the results of the blowup analysis in Fig. 3. See figure caption for further description. Guiding these manifolds along and one obtains the global manifolds and . In particular, by considering the variational equations of (1.11) along the following was shown in [24].

Lemma 1.3.

and intersect transversally along if and only if .

By regular perturbation theory, the extension of the slow manifolds and by the flow are therefore smoothly -close to and , respectively, in compact subsets of the chart . Hence, as a consequence of Lemma 1.3, for every there exist a transverse intersection of and which is -close to in fixed compact subsets of the scaling chart. In general, recall Remark 1.1, it seems that there do not exist any results on how far this perturbed ‘weak canard’ extends and whether ‘it’ (being nonunique) actually reaches the true Fenichel slow manifolds and . The situation is different for . First and foremost, and always intersect transversally along this orbit. Consequently, always perturbs as a ‘strong maximal canard’ for all , and this perturbed version always reaches the Fenichel manifolds. This latter property is a consequence of the repelling nature of , ‘forcing’ () and the forward (backward) flow (, respectively) to coincide near this object.

1.2. Main result

Using a Melnikov approach, it was shown in [28, Theorem 3.1] that a transcritical bifurcation of the intersection of and occurs along for any odd , . As a result, additional (secondary) ‘canards’, connecting with , exist near , for all by regular perturbation theory. In this paper, we prove the existence of a pitchfork bifurcation for . We then have the following complete result regarding the bifurcations of ‘canards’ for (1.11):

Theorem 1.4.

Consider any and let be so that

Set and let

| (1.14) |

be the bifurcation equation (to be defined formally below in (2.17) locally near ) where each solution corresponds to an intersection of and . In particular, for all due to the existence of the connection . Then

-

(1)

For , (1.14) is locally equivalent with the transcritical bifurcation:

(1.15) -

(2)

For , (1.14) is locally equivalent with the pitchfork bifurcation:

In each case, the local conjugacy satisfies and

| (1.16) |

Theorem 1.4 item (1) is covered by [28]. In particular, it is shown (see [28, Propositions 3.2 & 3.3]) that

which produces (1.16) by singularity theory [10]. We will therefore only prove Theorem 1.4 item (2) in the following. Notice, however, that in [28], the Melnikov function is defined for all sufficiently small, measuring the intersection of and directly (rather than measuring the objects and ). Nevertheless, seeing that the bifurcations in Theorem 1.4 are for the system, we will in this paper just focus on (and will only describe the perturbation of transverse intersection points into , see e.g. Remark 4.3 and Remark 4.5).

1.3. Overview

The remainder of the paper is organized as follows: In the next Section 2, we review the Melnikov theory in [28] in further details and extend this approach to time-reversible systems, see also [13]. The result is collected in Theorem 2.8. This is relevant for (1.11), since this equation is time-reversible with respect the following symmetry

| (1.17) |

This reduces the proof of our main result, Theorem 1.4 item (2) on the pitchfork bifurcation, to evaluating two integrals; one of which is already covered by [28], while the other one is the ‘third order’ Melnikov integral mentioned above. We evaluate these integrals by characterizing the manifolds and locally through solutions of ‘higher order variational equations’ rather than, how it is done in [18], their (implicit) formulation through integral equations. We describe our approach further in Section 2.2 and how these variational equations can be solved upon reduction to an inhomogeneous Weber equation. In this section, we also present a general class of systems, that include the folded node normal form, the Falkner-Skan equation and the Nosé equations, for which we can show, see Theorem 2.9, that our method produces closed form expressions of the appropriate Melnikov integrals. These results rely on properties of Hermite polynomials , . All information on these orthogonal polynomials that is relevant to the present manuscript is available in Appendix A.

The proof of Theorem 1.4 is presented in Section 3 below, see Lemma 3.4 proven towards the end of the section. We show that our expressions agree with the computations in [18, App. A] in Appendix B. Next, in Section 4 we will use the time-reversible setting and the blowup approach to show that the additional intersections produced by the pitchfork bifurcation do not reach the actual Fenichel slow manifolds for any , see Proposition 4.4 and Remark 4.5. They do therefore not produce ‘true’ canards. This is in contrast to the case where it is known that true ‘secondary’ canards are produced for every and . We also provide a new geometric explanation for this property in Section 4, see Proposition 4.2. Although these statements about canards are probably known to most experts in the field, we believe that we present the first rigorous proofs of these facts. In our final Section 5, we consider some other equations: the two-fold, the Falkner-Skan equation (1.3), and the Nosé equations (1.4), for which our time-reversible Melnikov approach in Section 2 is also applicable. In particular, for the Falkner-Skan and for the Nosé equations we provide a new geometric proof of the emergence of symmetric periodic orbits from infinity in these systems. For the Nosé equations, we show that for periodic orbits only emerge for , a result that escaped [23]. We conclude the paper in Section 6.

2. A Melnikov theory for time-reversible systems

The reference [27] describes a Melnikov theory for connection problems of nonhyperbolic points at infinity. In this section, we will review this approach in the context of time-reversible systems. For simplicity, we restrict to and consider a general smooth ODE

| (2.1) |

for , depending on a parameter , and assume the following:

-

(H1)

There exists a time-reversible symmetry

(2.2) with being an involution: , being the identity matrix in , such that

for all and all .

Therefore:

| If is solution of (2.1) then so is . |

As is standard, we say that an orbit with parametrization , which is a fix-point of the symmetry: for all , is ‘symmetric’. On the other hand, in general two orbits , for which , is said to be ‘symmetrically related’.

Furthermore, we say that a solution of (2.1) has algebraic growth for if there exists a such that for large enough. Specifically, we define the Banach space

for fixed, see [27]. Similarly, a solution of (2.1) has algebraic growth for if for large enough. Accordingly, we define

We will suppress in and whenever it is convenient to do so.

Next, we assume

-

(H2)

For there exists a symmetric solution with parametrization , , of at most algebraic growth for , i.e. with large enough. Without loss of generality we suppose that

-

(H3)

There exists a three-dimensional smooth invariant manifold in the extended system

(2.3) Here denotes the center-stable manifold consisting of all solution curves of (2.1) near (and including) (in a sense specified below) for which , for large enough.

is foliated by two-dimensional invariant manifolds of (2.1) for fixed values of , sufficiently small.

By (H1) and (H3), there exists a center-unstable manifold

| (2.4) |

consisting of all solution curves of (2.1) near (and including) for which .

-

(H4)

Let . Then for there exists a one-dimensional linear space such that

is a two-dimensional subspace.

(H4) implies that the manifolds and intersect tangentially along for . In fact, seeing that we have

Lemma 2.1.

The following statements are equivalent:

-

(1)

(H4) holds.

-

(2)

and the intersection of and along is tangential.

-

(3)

is an invariant subspace for : .

-

(4)

The variational equation along for :

(2.5) where , has two linearly independent solutions and for which .

Proof.

Next, following [28] let

| (2.6) |

Then . Let , and be unit vectors spanning , and , respectively, and denote the coordinates of any with respect to this basis by . Fix small and let be the ball of radius centered at . We then define a local section transverse to at by

Notice that – in the -coordinates – is contained within the -plane. Next, we write following [27] such that

| (2.7) |

where . Also and notice that (2.5) is the variational equation along . Furthermore:

Lemma 2.2.

for all .

Proof.

Follows directly from the time-reversible symmetry of , recall (H1). ∎

Let be the state-transition matrix of (2.5). Then by (H3) and (H4) there exists a continuous projection such that

and

for all . Furthermore, if then

| (2.8) |

and it follows that

| (2.9) | ||||

for some , and all , see e.g. [27, 26]. By assumption (H1), Lemma 2.2 and (2.9) we also have:

Lemma 2.3.

is symmetric in the following sense:

Also, and are continuous projection operators such that

for all .

Proof.

Straightforward calculation. ∎

Consider the adjoint equation of (2.5):

| (2.10) |

and notice that

| (2.11) |

is a time-reversible symmetry for (2.10) by (H1). Then

Lemma 2.4.

Let be a solution of (2.10). Then decays exponentially for if and only if .

Proof.

Standard, see [27]. ∎

In the following, we fix a specific by setting . Since is a state-transition matrix of (2.10), we can then write as

| (2.12) |

We now have the following important result.

Lemma 2.5.

and are one-dimensional invariant subspaces of and , respectively. Hence; there exists , , such that

where for .

Proof.

First, regarding the -invariance of : The solution of (2.11) is exponentially decaying for . Clearly, the symmetrically related solution satisfies the same properties, and hence by Lemma 2.4; the -invariance of therefore follows. Next, since is symmetric it follows by differentiation with respect to that . But then since is invariant with respect to , recall Lemma 2.1 item (3), and , the statement about also follows from a straightforward calculation. ∎

In fact, in the -coordinates

| (2.13) |

Next, for (2.7), it can by variation of constants – following [27] – be shown that , with , if and only if there exists a such that

| (2.14) |

This enables an analytic characterization of the (nonunique) invariant manifold , which is essential for the Melnikov approach, as follows. Let the mapping be defined on so that is the right hand side of (2.14) and consider a sufficiently small neighborhood of . Then, upon possible modification (or cut-off) of (and therefore of in (2.7)), as in center manifold theory [3], we obtain for each , a unique fix-point of : , see [27]. Henceforth we will assume that such a modification of (and therefore of ) has been made. It is also standard, see also [27], to show that is smooth, with each partial derivative belonging to for large enough. In this way,

Remark 2.6.

In our examples, including (1.11), the invariant manifolds will be obtained, not as fix-points of (2.14), but as center manifolds upon appropriate Poincaré compactification. For the analysis of the implications of the bifurcations of , it will be important to study the reduced problem on such center manifolds. For the Falkner-Skan equation and the Nosé equations the ‘selection’ of these nonunique manifolds will be crucial to our analysis.

2.1. The Melnikov function

For sufficiently small, we write and locally within the -plane as smooth graphs

| (2.15) |

and

| (2.16) |

respectively, over . Following [27], we then define the Melnikov function as

| (2.17) |

Clearly, a root of corresponds to an intersection of and and, hence, to an intersection of and . Furthermore, the intersection is transverse if and only if the root is simple. We now prove the following.

Lemma 2.7.

| (2.18) |

Proof.

Following (2.17), we simply have to show that

| (2.19) |

for all and . We will show this using the integral representation (2.14) as follows. Let be the fix-point of the mapping , with being defined as the right hand side of (2.14), so that for all and within in the -coordinates. Then so that with

writing the right hand side in the -coordinates, recall (2.13). Since , we conclude from (2.16) that

This shows (2.19), seeing that . ∎

Now, we are ready to present the following, final result on the Melnikov integral, which is a translation of [27, Theorem 1] to the time-reversible setting in .

Theorem 2.8.

Let be the solution of (2.7) with initial conditions

| (2.20) |

with respect to the -coordinates, on within . Then

| (2.21) |

2.2. A recipe for computing appropriate Melnikov integrals

We can use (2.21) to describe the bifurcations of heteroclinic connections of and , provided that we can determine the partial derivatives of . We now describe a set of assumptions, covering all of the cases we study below, where we can describe a specific procedure for doing this. We start with the following.

-

(H5)

Suppose that for all and all .

Upon a linear change of coordinates, we may also suppose without loss of generality that is diagonal, recall (2.13).

-

(H6)

Suppose that .

Notice that is symmetric with respect to this .

-

(H7)

Suppose that is quadratic.

We can then show that all relevant Melnikov integrals can be evaluated in closed form.

Theorem 2.9.

Suppose (H3) and (H5)-(H7).

-

(1)

Then , upon scaling and if necessary, takes the following form

(2.24) with each coefficient depending smoothly upon the parameter .

-

(2)

Furthermore, let

Then (H4) is satisfied if and only if .

-

(3)

Next, let be so that and consider as in (2.21). Then for all and we have the following:

-

(a)

Suppose . Then , and , see (2.21), is an even function, so that for all . Furthermore, the following partial derivatives of can be evaluated in closed form:

If these quantities are nonzero, then the bifurcation equation is locally equivalent with the pitchfork normal form.

-

(b)

Suppose . Then , . In this case, the following partial derivatives can be evaluated in closed form

If these quantities are nonzero, then the bifurcation equation is locally equivalent with the transcritical normal form.

-

(a)

Proof.

Regarding (1): The general form in (2.24) is a simple consequence of by (H5), for all and all by (H6). Furthermore, we conclude, using a Poincaré compactification and center manifold theory, that (H3) implies that the term in the first component of satisfies and subsequently that there is no term in the second component of . Seeing that , we finally obtain (2.24) by scaling and as follows: , .

Next regarding (2): The general form (2.24) produces

| (2.25) |

But then, upon differentiating the first equation for in the variational equation (2.5) one more time with respect to , we can write the equation for as a Weber equation:

| (2.26) |

where the second order operator is defined by the general expression:

| (2.27) |

for any . From , and can be determined by successive integration of

| (2.28) | ||||

We have.

Lemma 2.10.

Let , , denote the th degree Hermite polynomial. Then for all non-negative integers and , the following holds

| (2.29) |

In particular,

| (2.30) |

Therefore for there exists by (2.30) an algebraic solution of (2.26). Inserting this solution into (2.28) produces, upon using (A.1) and (A.2) in Appendix A, an algebraic solution of (2.5):

| (2.31) |

is then a consequence of Lemma 2.1, see item 4. On the other hand, if then there are no algebraic solutions of (2.26), see e.g. [1], and therefore (H4) does not hold, see again Lemma 2.1 item 4. This completes the proof of (2).

To finish the proof, we just need to verify the claims about , and the partial derivatives of at in item (3). For this we first determine . Suppose that . Then a simple computation shows that the adjoint equation can be written as a second order equation for :

Substituting gives

recall (2.27), upon dropping the tilde. Using (A.1), we obtain the following expression for :

| (2.32) |

for some constant , ensuring that has length . The statements regarding and are then simple consequences of (2.31) and (2.32), recall Lemma 2.5.

Regarding the partial derivatives of , we focus on and the closed form expression for in (3a). Both and in (3b) are similar, but simpler, and therefore left out. Notice also that the statements about the local equivalence with the pitchfork and the transcritical normal form follows from singularity theory, see e.g. [10].

Let

| (2.33) |

Notice, by linearization of (2.14) using , it follows that is determined by an appropriate normalization of (2.31). Then by (2.32) we conclude that is a linear combination of terms of the following form

| (2.34) |

for . Obviously, this linear combination can be stated explicitly in terms of (2.24). However, the details are not important here. Next, suppose that is a finite sum of Hermite polynomials:

| (2.35) |

with being a finite index set and , for any . Then upon inserting (2.35) into (2.34) we obtain a linear combination of terms of the following form

| (2.36) |

with and . Again, the details are not important. However, each term of the form (2.36) can be determined in closed form using (A.7) and the statement of the theorem therefore follows once we have shown (2.35). For this we insert into (2.7) and differentiate the resulting equation twice with respect to . We then evaluate the resulting expression at and again use that . This gives a linear inhomogeneous equation for of the following form

By (2.25) we can therefore write the equation for as a second order equation and obtain an inhomogeneous Weber equation:

| (2.37) |

Notice that by (2.31) the right hand side of (2.37) is a sum of products of Hermite polynomials. The product rule in (A.7) in Appendix A allows us to write this sum of products as a sum of Hermite polynomials only. A simple calculation, using (A.2), then shows that this sum only consists of Hermite polynomials of even degree. We can then solve (2.37) using Lemma 2.10. In particular, by linearity and the fact that and , it follows from (2.29) that there exists an algebraic solution of (2.37) of the form

for a finite index set and , . This is , since (a) it has the desired algebraic growth and (b) . The latter property (b) is a consequence of for each . Upon integrating the equations for and we obtain a solution of the form (2.35). This completes the proof of Theorem 2.9.

∎

Remark 2.11.

The general procedure for evaluating , described in the proof above, can essentially be summarized as follows:

-

•

Step (a). Insert into (2.7) and differentiate the resulting equation twice with respect to . This characterizes as a solution of a higher order variational equation.

-

•

Step (b). This equation can by (H5)-(H7) be reduced to an inhomogeneous Weber equation, see (2.37), with right hand side as a finite sum of products of Hermite polynomials.

- •

- •

In principle, this procedure can be extended to cases where is a polynomial of higher degree. It is still possible to reduce the equation for to an inhomogeneous Weber equation with a right hand side consisting of a sum of Hermite polynomials. However, I have not managed to find an appropriate general setting for this, where one can show that this right hand side does not involve . These terms belong to the kernel of , recall (2.30), and we can therefore not apply Lemma 2.10, as described in step (c), to inhomogeneous terms of this form. There are similar issues related to formalising the procedure iteratively to obtain closed form expressions for higher order derivatives of and .

Remark 2.12.

In [18], in the case of the folded node normal form, a more implicit, integral representation of is obtained by differentiating the fix-point equation , with defined by the right hand side of (2.14). Inserting this expression into the expression for gives a double integral, which (presumable) can be evaluated in Mathematica. The reference [18] computes all values up to for the folded node. ( We compare these values with our closed form expressions in Appendix B.) However, it is unclear if it is possible to evaluate such double integral directly.

3. Application of Theorem 2.8 to the folded node: Proof of Theorem 1.4

In this section, we now prove Theorem 1.4. For this, we follow the recipe in Section 2.2, summarized in Remark 2.11. But first we follow [28] and rectify , recall (1.12), to the -axis by introducing

| (3.1) | ||||

so that

| (3.2) |

using – for simplicity – the same symbol for the same object in the new variables. Notice that [18] rectifies in a slightly different way, see Appendix B. Inserting (3.1) into (1.11) produces

| (3.3) | ||||

which we, see also [28, Eq. (2.18)], will study in the following. The system (3.3) is time-reversible with respect to the same symmetry as in (1.17). It is easy to see that (3.3) satisfies the assumptions (H5)-(H7) and Theorem 2.9 applies. In particular, we have

We will therefore apply the procedure used in the proof of this result, specifically see Theorem 2.9 item (3a) and Remark 2.11, to (3.3). This will enable a proof of Theorem 1.4.

In the following, let

Then by Lemma 1.3 and the analysis in [28] the assumptions (H1)-(H4) are satisfied. At this stage, we keep general. For the results in the following are therefore covered by [28]; the only exception is that we exploit the symmetry to simplify some of the expressions.

Writing gives

| (3.4) | ||||

where

| (3.5) |

In comparison with (2.7), ‘’ for (3.4) is really , but it is useful to allow for a slight abuse of notation and let here refer to the first nontrivial coordinate function only. Setting (ignoring the nonlinear terms) in (3.4) produces the variational equations about

| (3.6) |

By differentiating the first equation for in (3.6) with respect to , we obtain a Weber equation for :

recall (2.27). For , it has an algebraic solution:

| (3.7) |

Inserting (3.7) into the remaining equations for and , we obtain the following state-transition matrix of (3.6):

| (3.8) | ||||

| (3.9) |

see also [28, Eqns. (3.14)-(3.15)]. Following the notation in [28], the asterisks denote a separate linearly independent solution that we do not specify and which will play no role in the following. Setting in the expressions for above, it follows that the -plane has the following decomposition:

where

| (3.12) | ||||

| (3.15) |

Proposition 3.1.

As a corollary, we have the following.

Corollary 3.2.

Consider . Then solutions of bifurcating from correspond to symmetric solutions of (3.4), i.e. they are fix-points of the time-reversible symmetry .

Proof.

Follows from (3.18) and the fact that any solution of in this case lies within , corresponding to , being the fix-point set of the symmetry . ∎

In contrary, when bifurcating solutions come in pairs (as a pitchfork bifurcation) that are related by the symmetry.

Now, finally by Theorem 2.8 we have.

Lemma 3.3.

Let be the solution with in the -coordinates. Then and

| (3.21) |

Proof.

Proof of Theorem 1.4 item (2).

We now write , . By Proposition 3.1, items (1) and (2), it follows that

| (3.22) |

for all and all . Next, we have the following lemma.

Lemma 3.4.

For with the following expressions hold:

| (3.23) | ||||

| (3.24) |

Let be the elements of the sum in (3.24):

for . Then for every

and

| (3.25) |

for all .

We turn to the proof of Lemma 3.4 once we have shown that Lemma 3.4 implies Theorem 1.4. For this, we first estimate the negative terms (where ) of the sum in (3.24) using (3.25) to obtain the following positive lower bound,

| (3.26) |

of , with the right hand side being the sum of only positive terms. Consequently, the expressions (3.22), (3.23), (3.24) – together with singularity theory [10] – proves our main result Theorem 1.4 item (2) on the pitchfork bifurcation.

∎

Proof of Lemma 3.4.

Let be as described. Recall, that it has algebraic growth as , and that for all since is a solution for all . Furthermore, by differentiating (3.4) with respect to and setting , we obtain the following equation

with , recall (2.33). Here is given in (3.6) with . Consequently, by (3.9) we have

| (3.27) |

see also [28]. Let , recall (2.33), denote the second partial derivative of . We now follow the steps in Remark 2.11.

Step (a). By differentiating (3.4) once more with respect to and setting we obtain a ‘higher order variational equation’

| (3.28) |

We have the following.

Proof.

Using that is an even function, the formula in (A.6) in Appendix A then produces the desired expression (3.23) for in Lemma 3.4.

To prove the remaining expression (3.24) in Lemma 3.4 for , we determine , which is the only remaining unknown in the expression (3.30).

Step (b). We do so by first writing (3.28) as an inhomogeneous Weber equation for :

| (3.31) |

recall the definition of second order linear differential operator in (2.27).

Step (c). We then use Lemma 2.10 to solve the linear, inhomogeneous equation (3.31) for the algebraic solution with , once we have written the right hand side of (3.31) as a finite sum of Hermite polynomials. For this we use (A.7):

Lemma 3.6.

The following holds true for any :

Proof.

Calculation. ∎

Consequently, we have

Lemma 3.7.

The following holds true for any :

| (3.32) | ||||

| (3.33) |

Proof.

Step (d). We then have.

Lemma 3.8.

The following holds for any :

Proof.

To show (3.25) we simply expand the binomial coefficients in the expression for and obtain

where the numerator and denominator both consist of factors. We simplify half of these factors by dividing up

We can write the last fraction as a product

where each factor is for every . This shows (3.25) and we have therefore completed the proof of Lemma 3.4. ∎

4. Secondary canards: a complete picture

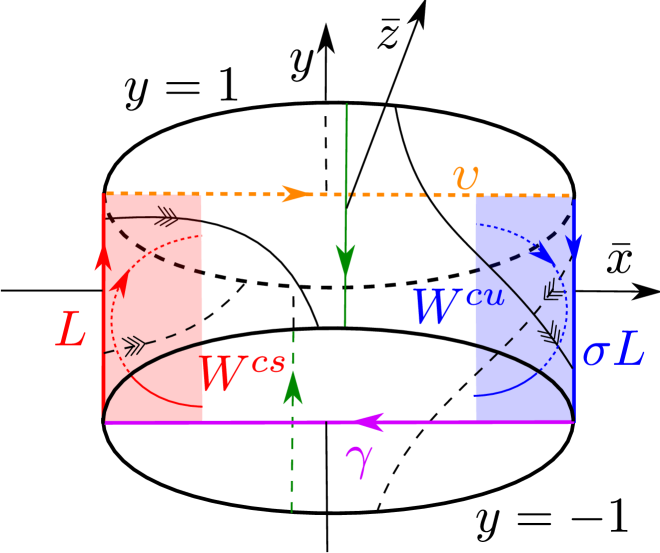

In Fig. 4 we present a sketch of the compactified version of (1.11) using the Poincaré compactification induced by (1.8). The diagram is therefore identical to Fig. 3, but with (and therefore ). Recall also that the three-dimensional hemisphere , is “flattened out” by projection onto the -space, so that the sketched two-dimensional-sphere corresponds to the “equator” of . On the other hand, everything inside is . In the following, we let act on as follows . This action is consistent with (1.17). The red and blue curves on the equator sphere correspond to the intersection with the critical manifold: , which away from has gained hyperbolicity, recall Fig. 3. Applying center manifold theory to these points gives rise to the local center manifolds and also illustrated as shaded surfaces extending into . (Recall, that these manifolds are (a) the ones obtained by restricting the manifolds and to the sphere and therefore (b) the ‘extensions’ of the critical manifolds and , respectively, onto the blowup sphere, recall Fig. 3. ) The manifolds and contain the strong and weak canards (orange and purple dotted lines, respectively), being heteroclinic orbits, within this framework, connecting partially hyperbolic points and , given by

with and , respectively, on the equator sphere with . Another simple calculation in the ‘’ chart shows that the points and are hyperbolic attracting and repelling nodes, respectively. They correspond to the intersection of the nonhyperbolic critical fiber of the folded node (in Fig. 1 this fiber coincides with the -axis) with the blowup sphere. On the other hand, by working in the chart ‘’ it follows that the points are fully nonhyperbolic. Notice also .

In the following, we write to mean that while is ‘sufficiently small’. We define similarly to mean that . Finally, will mean that is ‘sufficiently small’.

Recall that for (1.11), in (1.12) is the ‘weak canard’ written in the chart. This special orbit divides the center manifolds into unique and nonunique subsets. To see this, notice that the local center manifold for and is unique around the strong canard all up to the weak canard since these points coincide with the stable set of , see Fig. 4 and [28, Fig. 9]. We collect this result – using the -variables, recall (3.1) – as follows:

Lemma 4.1.

The local center manifold is unique on the side as the stable set of but nonunique for . Indeed, every point on the nonunique side of with is forward asymptotic to the hyperbolic and attracting node .

Proof.

Regarding the unique side of , we proceed as follows. In terms of the coordinates specified by the chart ‘’, the point is whereas is . The center manifold in (1.13) is therefore only unique for which upon coordinate transformation becomes , seeing that . The result then follows from the definition of in (3.1).

On the other hand, to verify the statement about , we blowup each to a sphere by setting

| (4.1) |

leaving untouched, where , . Only is relevant. Notice that these weights are the same as those used for blowing up the fold in , see [25]. The calculations are also essentially identical to those in [25], so we skip the details and just present the resulting diagrams, see Fig. 5 and Fig. 6 for the blowup of and , respectively. In these figures, the spheres , obtained from the blowup (4.1), are shown in green. The consequence of these blowups are then that each point on with , , is forward asymptotic to . Seeing that is a hyperbolic and attracting node, this means that is nonunique on this side of . ∎

Using the symmetry, we obtain a similar result for . In particular, every point on the nonunique side of with is backwards asymptotic to .

4.1. The transcritical bifurcation

Now, consider the transcritical bifurcation near any odd integer . Then by Theorem 1.4 item (1) and Corollary 3.2, we have a symmetric secondary canard for any . For , . Furthermore

Proposition 4.2.

The following holds for any :

-

(1)

For any , is backwards asymptotic to and forward asymptotic to . In this case, is nonunique.

-

(2)

For any , is backwards asymptotic to and forward asymptotic to . In this case, is unique as a heteroclinic connection.

Proof.

Firstly, the fact that is either (1): backwards asymptotic to and forward asymptotic to or (2): backwards asymptotic to and forward asymptotic to , is a consequence of being symmetric, recall Corollary 3.2. Similarly, the uniqueness of is a consequence of the uniqueness of the center manifolds on one side of only, see discussion above and Lemma 4.1. To complete the proof, suppose that . ( is similar and therefore left out.) Therefore and by working with the normal form (1.15), recall also (1.16), we realise that intersects along . Let denote the intersection point. Then by (1.15)

| (4.2) |

We will now show that the -component of is negative for all sufficiently large. For this purpose, consider the first column of the state-transition matrix in (3.8)n=2k-1 and multiply this column by the nonzero number . This gives the following solution

| (4.3) |

of the variational equations (3.4) with an initial condition

| (4.4) |

along ; recall that is for . Using (A.5) we realise that the first component of (4.4) has the same sign as (4.2). Fix therefore large enough so that , say, for all . Such exists since is polynomial with positive coefficient of the leading order term . Then specifically, the -component of (4.3) is negative for all , and consequently for , by regular perturbation theory, the -component of the time forward flow of is also negative. This completes the proof since by Lemma 4.1, then belongs to the unique side of with being forward asymptotic to . See also Fig. 4. ∎

Remark 4.3.

Here we recall some basic facts about canards from [2, 24, 28]. Whereas the strong canard always persists as a true (‘maximal’) canard for any , connecting the Fenichel slow manifolds and , the perturbation of the weak canard for to a true (‘maximal’) canard is clearly more involved. In particular, there is no candidate weak canard on the critical manifold, but rather a funnel of trajectories tangent at to the weak eigenvector at the folded node. However, seeing that on the blowup sphere is asymptotic to and for fixed , see Proposition 4.2 (2), this secondary canard has the same asymptotic properties as and it therefore also perturbs into a true (‘maximal’) canard connecting the Fenichel slow manifolds and for , see also [28].

In fact, the secondary canards appearing for do not undergo additional bifurcations for . Therefore if satisfies for some , then there exists secondary canards for all , see [28, Proposition 4.1]. These canards divide the Fenichel slow manifold into bands -close (with respect to ) to the strong canard with different rotational properties [2]. These bands provide an explanation for mixed-mode oscillations, see also [4].

4.2. The pitchfork bifurcation

Next, we consider and the pitchfork bifurcation. Then by Theorem 1.4 item (2) there exists two secondary canards and for any (or ). For , .

Proposition 4.4.

The secondary canards and for are nonunique heteroclinic connections. One connects with while the other one connects with .

Proof.

Together Proposition 4.2 and Proposition 4.4 provide a rigorous and geometric explanation of [28, Fig. 17]. In this figure, ‘’ and the ‘TPB’s are points beyond which does not reach the fixed local version of , see (1.13).

Remark 4.5.

As in Remark 4.3, we will now describe the implications of Proposition 4.4 for . Fix and suppose without loss of generality that is the connection from to . For all , seeing that and are transverse along , this secondary canard produces, as for the transcritical bifurcation above, a connection between the extended manifolds and . But since for is asymptotic to in forward time, the perturbed ‘canard’ never reaches the Fenichel slow manifold . Instead it follows, upon blowing down, the nonhyperbolic critical fiber as . However, since is close to the strong canard for all sufficiently negative, we can flow the perturbed version backwards and conclude that it does in fact originate from the Fenichel slow manifold . Here it also divides the subset of between the secondary canard due to the bifurcation at and the rest of the funnel into regions of separate rotational properties through the folded node, see also [28, Proposition 2.5].

5. Other examples of time-reversible systems

In this section, we present a few other examples: The two-fold, the Falkner-Skan equation and finally the Nosé equations, of nonhyperbolic connection problems where our time-reversible version of the Melnikov theory in [27] can be applied to study bifurcations. Whereas our analysis of the two-fold is brief – postponing all of the details to future work – we do include complete, self-contained descriptions of the bifurcations of periodic orbits in the Falkner-Skan equation and the Nosé equations.

5.1. The two-fold: Bifurcations of ‘canards’

Singularly perturbed systems in that limit to the piecewise smooth two-fold singularity, see [11], also possess orbits that are reminiscent of weak and strong canards in the singular limit . In particular, upon blowup, the two-fold corresponds to a ‘’-singularity of a reduced problem on a critical manifold, having attracting and repelling parts on either side of . Upon desingularization, in much the same way as in (1.6), becomes a stable node with eigenvalues for a subset of parameters. The essential geometry is shown in Fig. 7, see further description in the figure caption. Notice the geometry is essentially different from the folded node, insofar that the attracting and repelling manifolds for the two-fold only ‘meet up’ at the point , whereas for the folded node they align along the fold line. Nevertheless, upon further blowup, [15] showed, see also [14], by working on a ‘normal form’, that center manifold extensions of slow-like manifolds for the two-fold also intersect along a ‘strong canard’ for all , as well as along a ‘weak’ one provided that . The equations in the associated scaling chart for take the following form

| (5.1) | ||||

see [14, Eq. (93)]. Here is any ‘regularization function’ satisfying and as . Associated with the strong and weak eigenvectors of , the system (5.1) has, under certain assumptions on the parameters of the system ( and ), two algebraic solutions and , respectively. These solutions each lie within sets of the form and their projections onto the -plane coincides with the strong and weak eigenspace, see further details in [15, 14]. Moreover, and are fixed by the time-reversible symmetry of (5.1) given by and correspond to ‘unbounded heteroclinic connections’ upon the compactification provided by the blowup for . Moreover, even though (5.1) does not fit our general framework in Section 2.2, the variational equations along can also be reduced to the Weber equation, see [14, Eq. (101)]. In particular, for each , this equation has an algebraic solution resulting in a bifurcation scenario similar to folded node, where ‘secondary canards’ (may) emerge. I expect that the details are very similar to the folded node above, see also the numerical exploration in [15, Section 8]. However, I also expect it to be slightly more involved due to the many parameters of the system. (In fact, it might be more advantageous to work with a different, further simplified, normal form, e.g. one derived from the ‘normal form’ in [11] based on the associated piecewise smooth Filippov system). I have therefore decided not pursue this problem further in the present manuscript.

5.2. The Falkner-Skan equation: Bifurcations of unbounded periodic orbits

In [22] it was shown for the Falkner-Skan equation (1.3) that periodic orbits bifurcate from each integer value of . As noted in [23], the proof is long, complicated and – to a large extend – not based upon dynamical systems theory. The aim of the following section, is therefore to give a simple proof using the Melnikov approach, in particular Theorem 2.8, and the recipe in Section 2.2, which is based upon – as is more standard in dynamical systems – invariant manifolds. See also [17], for a similar approach in this context. In this reference, however, periodic orbits are constructed through an analysis of a return mapping.

First we write the equation (1.3) as a first order system

| (5.2) | ||||

which possesses two special solutions:

and a time-reversible symmetry given by

Both and are symmetric orbits. It is easy to see, upon rectifying to the -axis, setting , that (5.2) satisfies the assumptions in Section 2.2, recall (H5)-(H7), respectively. In particular,

Theorem 2.9 therefore applies and we can evaluate the relevant integrals at bifurcations in closed form following the recipe outlined in Remark 2.11. To describe the global dynamics relevant for the bifurcations of periodic orbits, and obtain the invariant manifolds and , we will compactify the system. For our purposes I find it useful to just compactify , leaving untouched, by setting

| (5.3) | ||||

for . To describe the dynamics near the equator defined by , we consider the directional chart ‘’ defined by

| (5.4) | ||||

The smooth change of coordinates between the ‘’ chart, defined in (5.3), and the ‘ chart, given by (5.4), is determined by the following equations

| (5.5) | ||||

for . Using (5.5) we obtain the following equations in the ‘’ chart:

| (5.6) | ||||

upon multiplication of the right hand sides by , to ensure that – corresponding to under the coordinate map – is invariant. For this system, we notice that any point is a partially hyperbolic equilibrium of (5.6), the linearization having as a single nonzero eigenvalue. Therefore, by center manifold theory there exists a local repelling center manifold . A simple calculation, using the invariance of and , shows that it takes the following form

| (5.7) |

with a fixed sufficiently large interval and where is sufficiently small. Also, is a smooth function, also depending on . In terms of , takes the following form

valid for all sufficiently negative.

Inserting (5.7) into (5.6) gives the reduced problem on :

| (5.8) | ||||

upon desingularization through division of the right hand side by . Notice that for and all sufficiently small. In particular, and are saddles, with the orbit , being a heteroclinic connection under the flow of (5.8). For later reference, let be the invariant set defined by

| (5.9) |

It becomes , on the cylinder.

By applying the symmetry, we obtain a local manifold for all sufficiently large. Combining this information we obtain the diagram in Fig. 8, see [21, Fig. 1] for a related figure.

The global manifolds and intersect along and . In particular, along we have the following

Lemma 5.1.

The manifold and intersect transversally along if and only if .

Proof.

We use Lemma 2.1 item (4). Consider therefore the variational equations about :

| (5.10) | ||||

which upon eliminating and , can be written as a Weber equation

| (5.11) |

recall (2.27). The result then follows from Lemma 2.10, see also proof of Theorem 2.9. In particular, for , we obtain the following algebraic solution of (5.10):

| (5.12) |

∎

Next, fix any and define by

Then we can define a local Melnikov function , the roots of which correspond to intersections of and near . Using Theorem 2.8, and proceeding as in the proof of Theorem 1.4, we obtain the following.

Proposition 5.2.

Let be so that

Then

-

(1)

For , is locally equivalent with a pitchfork bifurcation:

(5.13) -

(2)

For , is locally equivalent with the transcritical bifurcation:

(5.14)

In each case, the local conjugacy satisfies and

Proof.

See Appendix C. ∎

The bifurcations of and , described in the previous result, produce new transverse intersection for and every . Notice, however, that they will not always produce periodic orbits. Instead they may simply diverge (by following the invariant green curves in Fig. 8 defined by ). To give rise to periodic orbits, the intersections have to be symmetric (which rules out the pitchfork bifurcation, whose symmetrically related solutions diverge either as along the green curves in Fig. 8) and they have to be on the ‘right’ side so that they follow and . This is qualitatively very similar to the bifurcation of canards, recall Proposition 4.2 and Proposition 4.4. However, whereas for canards, the ‘interesting’ orbits, the true canards, appeared on unique sides of the invariant manifolds, we will see that for the Falkner-Skan equation and the Nosé equations, described below, the ‘interesting’ periodic orbits now appear on the nonunique sides of the manifolds. To obtain closed orbits we will have to fix copies of the center manifolds. We do so by using the fix-point sets of the symmetries.

In fact, we obtain a new proof of the following result on the bifurcation of periodic orbits from infinity, see [22], now based upon bifurcation theory and invariant manifolds.

Theorem 5.3.

Let be the (singular) heteroclinic cycle obtained from concatenating (a) , (b) the ‘segment’ , , recall (5.9) in the ‘’ chart, (c) , and finally (d) , i.e. the symmetrically related version of the segment defined in (b). Then symmetric periodic orbits bifurcate from for each .

In further, details let (so that ). Then symmetric periodic orbits only exist (‘locally’ to ) for .

Proof.

The manifolds and are (again) nonunique. We select unique copies as follows: Consider the strip defined by with . Notice that . We then select a unique copy of on the side of by flowing this strip backwards (where becomes attracting). Obviously, we let be the symmetrically related version of this fixed manifold.

Now, the transcritical bifurcation (5.14) produce a secondary intersection of and for all so that . In particular, we first note – following (C.4) in Appendix C – that intersects along the -axis. Let denote this intersection point where . Consider so that . Then by (5.14) we have

| (5.15) |

Consider now the solution (5.12)n=2k of the variational equations (5.10), repeated here for convenience

| (5.16) |

with initial condition

| (5.17) |

By (A.5) in Appendix A, we realise that the sign of the second component of (5.16) coincides with the sign of (5.15). But then, since the second component of (5.16) is positive for all sufficiently large , we conclude that for follows for large enough. Subsequently, by following , see Fig. 8, we realise that returns to . Since we have fixed the manifolds to intersect in the strip , this intersection is of the form with as . But then upon applying the time-reversible symmetry, we obtain a closed orbit. The periodic orbit intersects the fix-point set of , defined by twice, once near at and once near at .

In the remaining cases ( and the ), the ‘secondary intersection’ diverge as either by following the green curves in Fig. 8 defined by . ∎

Remark 5.4.

Notice that the periodic orbits appearing for will rotate (or twist) around , the number of rotations, as for the folded node, being determined by . See Fig. 9 for examples, and the figure caption for further description. As for the folded node, and the twisting of the secondary canards around the weak one, these rotations around can be explained by the solutions (C.14) of variational equations, see [28] for further details.

5.3. The Nosé equation: Bifurcations of unbounded periodic orbits

The system (1.4) has two time-reversible symmetries given by

and

as well as one symmetry given by , the superscripts , and indicating the coordinates that are fixed by the transformation. Notice that and the group of symmetries of (1.4) is therefore the group, consisting of elements, generated by and . It is isomorphic to .

Furthermore, periodic solutions bifurcate from each integer value of , see [23]. For , it is known that periodic solutions only bifurcate at these values. In [22] they also show that for , (different) periodic solutions bifurcate for every , but they do not prove whether periodic solutions bifurcate from other values of , see remark following [23, Theorem 2]. In the following, we will prove this using our time-reversible version of the Melnikov theory:

Theorem 5.5.

For periodic solutions only bifurcate from ‘infinity’ for . In particular, periodic orbits only emerge for for each integer .

We will prove this theorem in the remainder of this section. For this purpose, it will be convenient to scale (1.4) in the following way: Let

and define and by

Then

| (5.18) | ||||

upon dropping the tildes again. For this system, there exists three special solutions of (1.4)

as well as

We introduce the Poincaré sphere by setting

By working in the charts defined by ‘’, , and applying the symmetries defined by , and we obtain the diagram in Fig. 10. Here we adopt the same visualization technique (by projection) used above: The outer sphere corresponds to the equator sphere defined by , whereas everything inside is . Notice, in particular, that the invariant manifolds and are obtained as local center manifolds in the charts ‘’, respectively. The reduced flow on these local manifolds, can be desingularized along to produce the dynamics indicated in the figure. The associated global manifolds and contain , and . These solution curves are shown in purple and orange. (Notice that these lines are actually not straight lines in the projection used in Fig. 10. The figure is therefore ‘artistic’.) We leave out the simple details. In particular, using thick lines, we visualize a (singular) heteroclinic cycle . It consists of (a) , (b) a segment (through the fully nonhyperbolic point at ) connecting ‘the end of’ with ‘the beginning of’ , (c) and finally . The periodic orbits of Theorem 5.5 will appear as bifurcations from this cycle through bifurcations of intersections of and . But notice the following:

Firstly, ‘new’ intersection of and may not produce periodic orbits. Similar to the bifurcation of secondary canards, these intersections may just converge to the points : , : as . Indeed, and are hyperbolic, being a source and a sink, for the desingularized slow flow on and , respectively. Notice that these manifolds are unique on the corresponding side of as stable and unstable sets of and , respectively. Consequently, to produce periodic orbits, additional intersections of and have to be on the ‘nonunique side’ of .

Secondly, there are other (singular) heteroclinic cycles. For example: (a) , (b) a piece of before (c) jumping off on a ‘fast’ connecting (shown in black near the green point ), (d) follow a separate piece on , (e) , etc. However, these cycles do not produce periodic orbits since they are not symmetric. The cycle is the only symmetric cycle.

To prove Theorem 5.5, we first realise, upon rectifying to the -axis, setting , that the system (5.18) satisfies the assumptions of Theorem 2.9. In particular,

Consequently:

Lemma 5.6.

The manifolds and intersect transversally along if and only if .

Proof.

Follows from Theorem 2.9, but for completeness notice the following: The variational equations about takes the following form:

| (5.19) | ||||

which upon eliminating and , can be written as a Weber equation:

| (5.20) |

recall (2.27). The result therefore follows from Lemma 2.10 and Lemma 2.1. Notice, in particular, that for we obtain, using (A.2) in Appendix A, the following algebraic solution of (5.19)

| (5.21) |

∎

Completely analogously to Section 5.2 for the Falkner-Skan equation, we fix any and define by

| (5.22) |

and let denote the resulting Melnikov function, the roots of which correspond to intersections of and near . Following Theorem 2.9 we can therefore evaluate the appropriate Melnikov integrals in closed form by using the recipe in Remark 2.11. In this way, we obtain the following result.

Proposition 5.7.

Let be so that

Then

-

(1)

For , is locally equivalent with a pitchfork bifurcation:

(5.23) -

(2)

For , is locally equivalent with the transcritical bifurcation:

(5.24)

In each case, the local conjugacy satisfies and

Proof.

See Appendix D. ∎

To complete the proof of Theorem 5.5, we first realise that when – in which case – then the roots of produce additional symmetrically related solutions, coexisting for . Working from the diagram in Fig. 10, we conclude, see also Proposition 4.4, that one of these solutions is asymptotic to whereas the other one is backwards asymptotic to . Hence no periodic bifurcate from . On the other hand, for , then the transcritical bifurcation produce for a ‘secondary’ intersection , with , of and . Since each is symmetric, it will be asymptotic to and for on one side of . On the other side, however, it will follow , recall Fig. 10 for large enough. To distinguish the two cases, we proceed as in the proofs of Proposition 4.2 and Theorem 5.3. In particular, we first note – following (D.6) in Appendix D – that intersects along the -axis. Denote the intersection point by and suppose that . Then and by (5.24),

| (5.25) |

Consider the solution (5.21) of (5.19), repeated here for convenience

| (5.26) |

with initial condition

| (5.27) |

By (A.5) in Appendix A, we realise that the sign of the first component in (5.27) coincides with the sign of (5.25). But then, since the second component of (5.26) is positive for all sufficiently large, we conclude that for follows for large enough. To construct periodic orbits, we fix by flowing the points near , of the form for large enough, backwards. This fixes a copy of . In this way, intersects for the first time in forward time in a point , where as . Since is symmetric with respect to the time-reversible symmetry , the first intersection in backwards time is at the point . But then upon applying the symmetry , we obtain a closed orbit that approaches the singular heteroclinic cycle as . The periodic orbit intersects four times: Once near at , once at , then near at , and then finally at .

Periodic orbits therefore only bifurcate from infinity for when , appearing for for each integer .

Remark 5.8.

For , and therefore only exists. In fact, bifurcates in a pitchfork-like bifurcation at in such a way that becomes a saddle for the reduced flow on . By following Theorem 2.9, and reducing the variational equations of (1.4) along to a Weber equation, it is again straightforward to show that and intersect transversally along if and only if .

6. Conclusion

In this paper, we have applied a time-reversible version of the Melnikov theory for nonhyperbolic unbounded connection problems in [27] to the bifurcations of canards in the folded node normal form. In particular, we proved – for the first time – the existence of a pitchfork bifurcation for . Our time-reversible setting also allowed for a new description of the ‘secondary canards’ emerging from the bifurcations at , see Section 4. The connection to the Weber equation as well as properties of the Hermite polynomials were essential to our proof of Theorem 1.4. But the results in Section 2.2, specifically see Theorem 2.9 and Remark 2.11, highlight that the Weber equation is ‘synonymous’ with quadratic, time-reversible systems satisfying (H4) and (H2) with the unbounded symmetric orbit linear in and independent of . This is also expected, as noted by [23], since the Weber equation is the ‘simplest’ non-autonomous equation with a non-trivial time-reversible symmetry. I believe that it is possible to obtain closed-form expressions for the Melnikov integrals in [18] related to the bifurcations of faux canards for the folded saddle singularity. Although these problems do not fit our general setting in Section 2.2, the Weber equation also appears naturally for these problems.

In Section 5, we also applied our approach to the Falkner-Skan equation and the Nosé equations. In particular, we provided a new proof of the emergence of periodic orbits, bifurcating from heteroclinic cycles at infinity, in these systems using more standard methods of dynamical systems theory. In particular, we showed that for the Nosé equations periodic orbits only bifurcate from , a result that had escaped [23]. In future work, it would be natural to use the geometric framework provided by this theory to study the emergence of chaos in these two systems.

Acknowledgement

I would like to thank Martin Wechselberger for his encouragement and for providing valuable feedback on an earlier version of this manuscript.

Appendix A Properties on the Hermite polynomials

Lemma A.1.

For every

| (A.1) | ||||

| (A.2) | ||||

| (A.5) |

and

| (A.6) |

where is the Kronecker delta.

Furthermore, for every , :

| (A.7) |

Finally, for every that satisfies the triangle property and for which :

| (A.8) |

If does not satisfy the triangle inequality or if , then the integral in (A.8) is .

Appendix B Comparison with [18]

In [18, App. A, p. 595] the third order Melnikov integral (3.24) is evaluated numerical for . However, we cannot compare the results directly since this reference considers ; in this case is the weak canard while is the strong one. Nevertheless, these two cases are obviously equivalent and we can map the system into the system, considered in the present paper, through the following transformation:

upon dropping the tildes. Specifically, this transformation maps and for into and for , respectively. But [18] also rectifies (which is for ) in a slightly different way. A simple computation shows that in [18, Eq. (15)] is related to in (3.1) as follows:

| (B.1) | ||||

upon also replacing by . Let be the Melnikov function in [18, Proposition 29] for and . Then from (B.1) and [18, Eq. (89)] it follows that:

where is the Melnikov function used in the present paper. Hence,

| (B.2) |

In Table 1, we compare each side of this equation, using our analytical expression (3.24) on the left hand side, whereas on the right hand side we use the numerical values in the table on [18, p. 595]. See further explanation in the table caption. We conclude that the results are in agreement (and attribute the tiny differences, indicated in red, to round off errors).

Appendix C The Falkner-Skan equation: Proof of Proposition 5.2

Let be defined as . Then we have

where

upon dropping the tildes. Then by (5.12), we obtain the following regarding the state transition matrix:

| (C.1) |

Consequently,

| (C.4) | ||||

| (C.7) |

and hence

| (C.10) |

Consequently, for , is an odd function for every . On the other hand, for roots of correspond to symmetric solutions, being fixed with respect to the symmetry . Furthermore, using

which follows from a simple calculation, we obtain

| (C.13) |

We now focus on , which is easier, and prove the transcritical case. The details of and the pitchfork are lengthier, but similar to the details of the proof of Theorem 1.4 item (2), see also Remark 2.11, and therefore left out.

Let therefore , such that , and write . Following (C.1), we have

| (C.14) |

Then upon differentiating (C.13) with respect to and we have

using (C.1) as well as (A.5) and (A.6) in Appendix A. Similarly, by differentiating (C.13) twice with respect to we have

where

using (C.14). To compute these integrals we use (A.8) in Appendix A and obtain the following expression

using (A.5), and, after some simple calculations,

Consequently,

By singularity theory [10] this proves the transcritical bifurcation and the local equivalence (upon replacing by ) with the normal form (5.14).

Appendix D The Nosé equations: Proof of Proposition 5.7

Let . Then

where

| (D.1) | ||||

upon dropping the tildes. By (5.21), we can compute the following relevant quantities:

| (D.2) | ||||

| (D.3) |

for some (unspecified) constant matrix (to ensure that ), which will not be important in the following, and consequently

| (D.6) | ||||

| (D.9) |

with respect to the symmetry , and hence

| (D.12) |

Consequently, for , is an odd function for every . On the other hand, for roots of correspond to symmetric solutions, being fixed with respect to the symmetry . Furthermore, using

which follows from a simple calculation, we obtain where

| (D.15) | ||||

| (D.18) |

As described in Theorem 2.9, we are able to evaluate these integrals by following the procedure in Remark 2.11:

Lemma D.1.

Let be so that

Then

-

(1)

For , the following holds

Furthermore, let

for . Then

-

(2)

For , then

and

Proof.

We simply differentiate the expressions (D.15) and (D.18) and use (D.1),

| (D.19) |

by (D.3) and (D.2), where . Following Remark 2.11, see step (a), we then characterize using the higher variational equations:

By the remaining steps b,c,d we obtain the results. The details are identical to Lemma 3.4 and therefore left out. ∎

References

- [1] M. Abramowitz and A. Stegun. Handbook of Mathematical Functions, volume 55. National Bureau of Standards Applied Mathematics Series, Washington, DC, 1964.

- [2] M. Brøns, M. Krupa, and M. Wechselberger. Mixed mode oscillations due to the generalized canard phenomenon. In W. Nagata and N. Sri Namachchivaya, editors, Bifurcation Theory and Spatio-Temporal Pattern Formation, volume 49 of Fields Institute Communications, pages 39–64. American Mathematical Society, 2006.

- [3] J. Carr. Applications of centre manifold theory, volume 35. New York: Springer-Verlag, 1981.

- [4] M. Desroches, J. Guckenheimer, B. Krauskopf, C. Kuehn, H. M. Osinga, and M. Wechselberger. Mixed-mode oscillations with multiple time scales. Siam Review, 54(2):211–288, 2012.

- [5] M. di Bernardo, C. J. Budd, A. R. Champneys, and P. Kowalczyk. Piecewise-smooth Dynamical Systems: Theory and Applications. Springer Verlag, 2008.

- [6] V. M. Falkner and S. W. Skan. Solutions of the boundary-layer equations in aerodynamics. Philosophical Magazine, 12:865–896, 865–896, 1931.

- [7] N. Fenichel. Persistence and smoothness of invariant manifolds for flows. Indiana University Mathematics Journal, 21:193–226, 1971.

- [8] N. Fenichel. Asymptotic stability with rate conditions. Indiana University Mathematics Journal, 23:1109–1137, 1974.

- [9] N. Fenichel. Geometric singular perturbation theory for ordinary differential equations. J. Diff. Eq., 31:53–98, 1979.

- [10] M. Golubitsky and D. G. Schaeffer. Singularities and Groups in Bifurcation Theory, volume 51. Springer, 1984.

- [11] M. R. Jeffrey and A. Colombo. The two-fold singularity of discontinuous vector fields. SIAM Journal on Applied Dynamical Systems, 8(2):624–640, January 2009.

- [12] C.K.R.T. Jones. Geometric Singular Perturbation Theory, Lecture Notes in Mathematics, Dynamical Systems (Montecatini Terme). Springer, Berlin, 1995.

- [13] J. Knobloch. Bifurcation of degenerate homoclinic orbits in reversible and conservative systems. Journal of Dynamics and Differential Equations, 9(3):427–444, 1997.

- [14] K. U. Kristiansen and S. J. Hogan. Resolution of the piecewise smooth visible-invisible two-fold singularity in R3 using regularization and blowup. Journal of Nonlinear Science, 29(2):723–787, 2018.

- [15] K. Uldall Kristiansen and S. J. Hogan. On the use of blowup to study regularizations of singularities of piecewise smooth dynamical systems in R3. SIAM Journal on Applied Dynamical Systems, 14(1):382–422, 2015.

- [16] M. Krupa and M. Wechselberger. Local analysis near a folded saddle-node singularity. Journal of Differential Equations, 248(12):2841–2888, 2010.

- [17] J. Llibre and M. Messias. Large amplitude oscillations for a class of symmetric polynomial differential systems in R3. Anais Da Academia Brasileira De Ciencias, 79(4):563–575, 2007.

- [18] J. Mitry and M. Wechselberger. Folded saddles and faux canards. Siam Journal on Applied Dynamical Systems, 16(1):546–596, 2017.

- [19] S. Nosé. A unified formulation of the constant temperature molecular-dynamics methods. Journal of Chemical Physics, 81(1):511–519, 1984.

- [20] F. W. J. Olver, D. W. Lozier, R. F. Boisvert, and C. W. Clark. Nist handbook of mathematical functions. Journal of Geometry and Symmetry in Physics, pages 99–104, 2011.

- [21] C. Sparrow and H. P.F. Swinnerton-Dyer. The Falkner-Skan equation II: Dynamics and the bifurcations of P- and Q-orbits. Journal of Differential Equations, 183(1):1–55, 2002.

- [22] H.P.F. Swinnerton-Dyer and C.T. Sparrow. The Falkner-Skan Equation I. The Creation of Strange Invariant Sets. Journal of Differential Equations, 1995.

- [23] P. Swinnerton-Dyer and T. Wagenknecht. Some third-order ordinary differential equations. Bulletin of the London Mathematical Society, 40(5):725–748, 2008.

- [24] P. Szmolyan and M. Wechselberger. Canards in . J. Diff. Eq., 177(2):419–453, December 2001.

- [25] P. Szmolyan and M. Wechselberger. Relaxation oscillation in ℝ3. Journal of Differential Equations, 200(1):69–104, 2004.

- [26] A. Vanderbauwhede. Bifurcation of degenerate homoclinics. Results in Mathematics, 21:211–223, 1992.

- [27] M. Wechselberger. Extending Melnikov theory to invariant manifolds on non-compact domains. Dynamical Systems, 17(3):215–233, 2002.

- [28] M. Wechselberger. Existence and bifurcation of canards in in the case of a folded node. SIAM Journal on Applied Dynamical Systems, 4(1):101–139, January 2005.